The Long Road to Stockholm

Imagine you are an economist with an idea that challenges conventional thinking. You spend years building a rigorous model, running statistical tests, gathering evidence. Your work is solid. You're ready to publish.

Then the real obstacle course begins.

The path to a Nobel Prize in economics starts long before Stockholm. It starts with the peer review system, where your work faces a trial by fire. And if you're fortunate enough to survive that gauntlet, you still face the Nobel Committee's own rigorous selection process. Few economists ever reach either threshold. Those who do have typically spent decades building an intellectual foundation so strong that it reshapes how we think about markets and human behavior.

The Peer Review Crucible

When you submit an academic paper to a top journal, your manuscript goes to an editor who decides whether it's even worth reviewing. If it passes that filter, the editor selects independent referees—typically two or three experts in your field—who examine everything: your methodology, your data, your statistical analysis, your logic. These referees check your work as though they're looking for errors. Because they are.

Referees are peers, which means they understand the frontier of the field deeply. They know what's been tried before. They know what's questionable. They know when a conclusion doesn't quite follow the evidence presented. Anonymous review means they can be blunt. They often are.

A paper gets rejected, or sent back for major revisions, or accepted with minor changes. Many papers cycle through this process multiple times before acceptance. Some never make it. The best journals have acceptance rates below twenty percent. For top-tier journals, they are often in single digits.

This isn't gatekeeping for its own sake. It's a quality filter. A paper that has survived rigorous peer reviews carries credibility. It means multiple experts have scrutinized your data and found it defensible. That matters when you're claiming to have discovered something true about how the world works.

Building Decades of Impact

Surviving peer review is only the foundation. The economics Nobel rewards work of genuine, lasting significance. The Committee isn't looking for a clever finding that excites the field for two years and then fades. It's looking for ideas that have fundamentally changed how economists think about a problem—and often, how the world conducts business as a result.

This requires time. Years, usually decades. Your papers need to accumulate citations. Other researchers need to build on your work. Your ideas need to influence policy or at least shape the intellectual consensus in your field. You need to publish more than a hundred papers, each one subjected to the same peer review scrutiny, each one adding to a body of evidence that becomes increasingly difficult to ignore.

The Nobel Selection Process

Once your body of work has achieved sufficient standing, you become eligible for consideration. But the Nobel Committee itself is extraordinarily selective. Each year, the Royal Swedish Academy of Sciences invites qualified nominators—previous Nobel laureates, leading economists at top universities, members of the Academy itself—to submit candidates. Hundreds of economists worldwide are nominated. Most will never win.

The Nobel Committee for Economic Sciences reviews these nominations and typically narrows the field to a shortlist. They may consult expert referees—international scholars who provide confidential assessments of the shortlisted candidates' work. The committee deliberates on the theoretical impact, the empirical rigor, and the real-world influence of each candidate's research. They rank candidates. They debate.

By late September, the committee makes a recommendation to the larger Economics Class of the Royal Swedish Academy. In early October, the Academy votes. The Royal Swedish Academy has roughly four hundred seventy members in total, but only the economists in its Economics Class—roughly eighty in number—cast ballots on the prize. A majority vote decides the winner. The decision is final and without appeal. The announcement comes with great fanfare.

It's another screening process, as rigorous as peer review itself. The Committee seeks work that has fundamentally changed how economists solve problems. That bar is extraordinarily high.

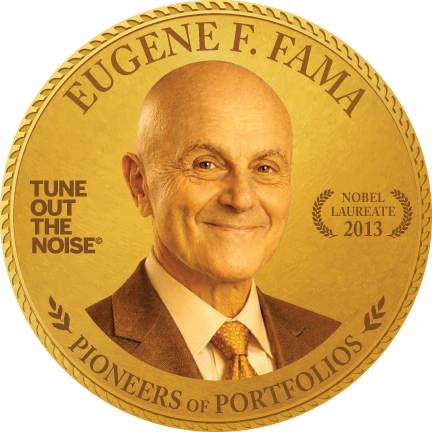

Eugene Fama and Forty-Eight Years

Eugene Fama first published his dissertation in nineteen sixty-five. He was a young economist at the University of Chicago, working under the supervision of Merton Miller—himself a future Nobel laureate. Fama's work was striking: he demonstrated that stock price movements are nearly impossible to predict in the short term, and that new information affects prices almost immediately. This finding contradicted decades of Wall Street conventional wisdom. The implication was widely viewed as radical: if markets are efficient, then picking stocks may be essentially futile. Professional stock pickers, on average, cannot beat the market through skill alone.

Eugene Fama first published his dissertation in nineteen sixty-five. He was a young economist at the University of Chicago, working under the supervision of Merton Miller—himself a future Nobel laureate. Fama's work was striking: he demonstrated that stock price movements are nearly impossible to predict in the short term, and that new information affects prices almost immediately. This finding contradicted decades of Wall Street conventional wisdom. The implication was widely viewed as radical: if markets are efficient, then picking stocks may be essentially futile. Professional stock pickers, on average, cannot beat the market through skill alone.

But one rigorous paper, however brilliant, doesn't win a Nobel Prize. Fama spent the next four decades building on that foundation. In nineteen seventy, he published "Efficient Capital Markets: A Review of Theory and Empirical Work," a comprehensive treatment that became the definitive statement on market efficiency. Over his career, Fama would publish more than a hundred papers. Each one was subjected to peer review. Each one added empirical evidence, refined theory, or challenged competing claims with data.

Other researchers tested his ideas. Some found anomalies. Fama and his collaborators investigated those anomalies rigorously. They developed the Fama-French three-factor model, then the five-factor model, explaining expected returns across stocks and asset classes with precision that previous theories could not match.

His work shaped not just academic thinking but market practice itself. Dimensional Fund Advisors, where Fama has served on the board since nineteen eighty-two, built an entire investment philosophy around his research. Index funds—now managing trillions of dollars globally—are widely associated with the intellectual foundation Fama fama helped develop.

A Conviction Held Since 1998

In nineteen ninety-eight, while conducting the research that would lead to the creation of Index Fund Advisors, I discovered Eugene Fama's work and recognized immediately the profound importance of his contributions to evidence-based investing. From the beginning, I claimed that Fama should win a Nobel Prize for his discoveries. It would take until two thousand thirteen for the Royal Swedish Academy to finally recognize his efforts.

I was so convinced of the importance of Nobel laureates to investors that in my book, Index Funds: The 12-Step Program for Active Investors, I titled Step Two "Nobel Laureates." In that step, I recounted the many Nobel laureates who contributed to the passive investing strategy that is the foundation of Index Fund Advisors' advice. Fama's efficient market hypothesis sits at the heart of that intellectual lineage.

Tune Out the Noise

When Academy Award-winning filmmaker Errol Morris directed the documentary Tune Out the Noise, he highlighted the impact of the discoveries of academics—and in particular Nobel laureates—in contributing to the ideas that led to the founding and investment strategy of Dimensional Fund Advisors and, ultimately, Index Fund Advisors. In that film, Morris interviewed Eugene Fama along with several other Nobel laureates, including Robert Merton and Myron Scholes, all of whom have long-standing ties to Dimensional.

(Watch Clips from the Movie ➤)

The importance of all the individuals in that film inspired the creation of my Tune Out the Noise coin series: eighteen commemorative coins honoring the contributions of the pioneers whose work transformed evidence-based investing.

The Prize Arrives

For nearly fifty years, Fama published, refined, tested, debated, and built. His ideas survived scrutiny. They accumulated evidence. They influenced practice. They changed how the world thinks about markets and investing.

In October of two thousand thirteen, the Royal Swedish Academy of Sciences voted. Roughly eighty economists in the Academy's Economics Class cast their ballots. Fama, along with Lars Peter Hansen and Robert Shiller, won the Nobel Prize in Economic Sciences. The citation read: "for their empirical analysis of asset prices."

Forty-eight years from his first publication to Stockholm. Fifteen years from my own recognition of his work to the Nobel Committee's official acknowledgment. That is how long it takes for an idea this consequential to be honored—and how long conviction must sometimes wait for vindication.

This material is provided for informational and educational purposes only and reflects the opinions of the author as of the date written. It is not intended as investment advice or a recommendation to buy or sell any securities or adopt any investment strategy. References to specific academic theories, firms, or investment approaches are for illustrative purposes only and should not be interpreted as endorsements or guarantees of future results. References to Dimensional Fund Advisors are provided for context; IFA may recommend Dimensional funds and may have business relationships with certain firms mentioned.

Any media, publications, or products referenced (including films or commemorative items) are separate from advisory services and do not constitute investment recommendations or testimonials.

All investing involves risk, including the loss of principal. Past performance and academic research findings are not indicative of future results. Index Fund Advisors, Inc. ("IFA") is a registered investment adviser.

X

X