Pioneers of Probability · Episode 6

This video is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. The historical and mathematical concepts discussed are intended to illustrate the development of probability theory and its relevance to investing. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. The examples provided are hypothetical and based on historical index data, not an actual investment. Index returns do not reflect the performance of any actual portfolio or the deduction of advisory fees. Content is AI assisted.

◆ The Question

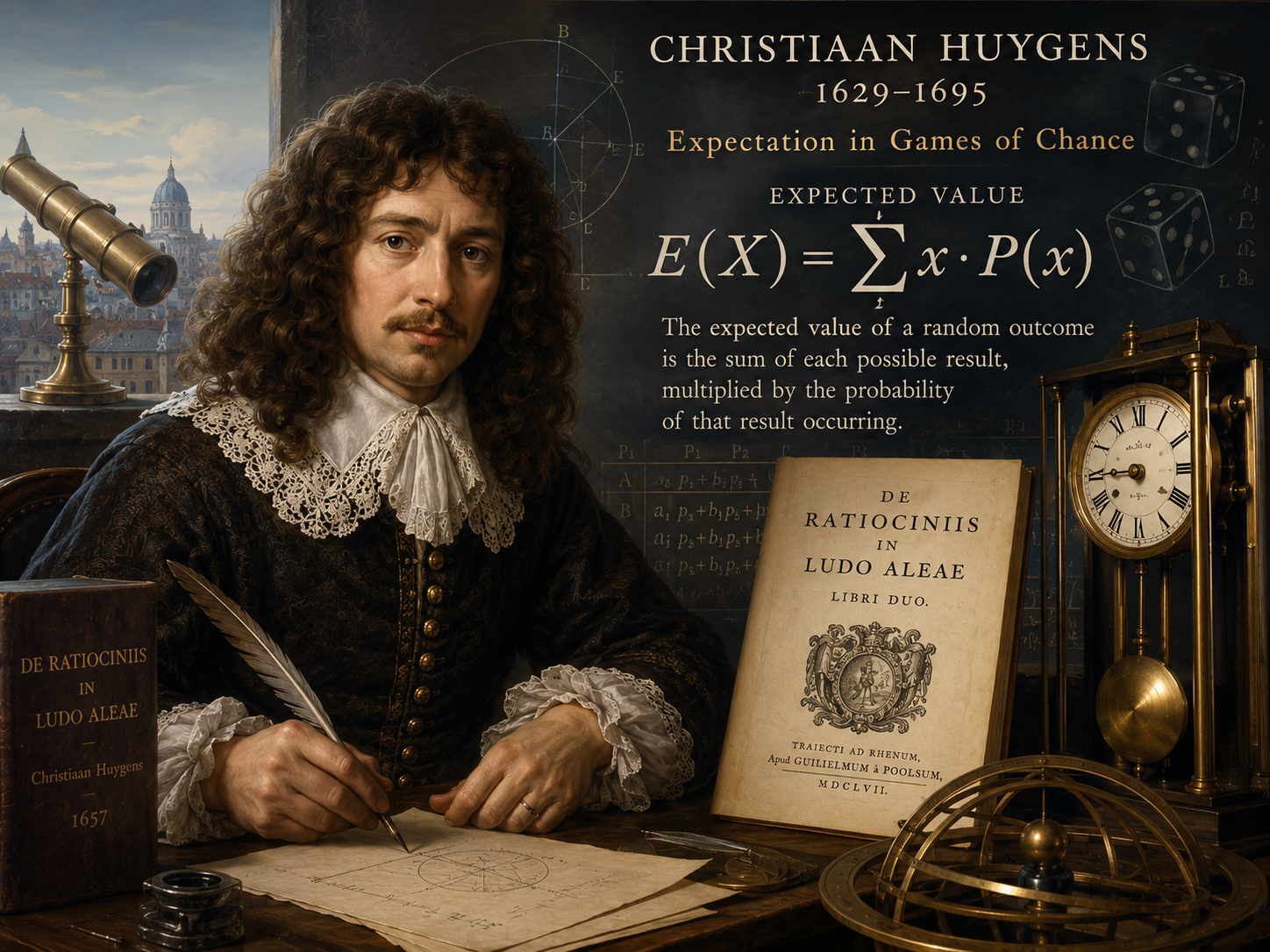

In 1655, a twenty-six-year-old Dutch scientist arrived in Paris for what was supposed to be a scientific visit. Christiaan Huygens came from one of the most distinguished families in the Netherlands — his father Constantijn was secretary and counselor to two successive Princes of Orange, a diplomat, a poet, and a friend of both René Descartes and the poet John Donne. The elder Huygens had educated Christiaan and his brothers at home with private tutors, then sent them to the University of Leiden and later to Breda to study law. Christiaan had studied law dutifully and then largely ignored it, devoting himself instead to mathematics, physics, and astronomy with the kind of single-minded intensity that tends to produce landmark results.

By the time he arrived in Paris, he had already done significant work in geometry and had begun grinding his own telescope lenses to a quality that surpassed anything available commercially. He was, in short, exactly the kind of young scientist who would have been invited into the mathematical conversation happening in Parisian salons. And in those salons, everyone was talking about the summer's sensation: the letters between Pascal and Fermat about the Problem of Points.

Huygens tried to get hold of the letters. He couldn't. The correspondence was still circulating privately, and the details had not been widely shared. So Huygens did what any serious mathematician confronted with a solvable problem would do: he worked it out for himself.

◆ The Insight

The Problem of Points was solved by the time Huygens returned to the Netherlands. But the solution that emerged from his independent reconstruction was not merely a replication of what Pascal and Fermat had done. Huygens went further. He generalized. Where Pascal and Fermat had solved specific instances of the gambling problem, Huygens asked a broader question: how should any uncertain prospect be valued?

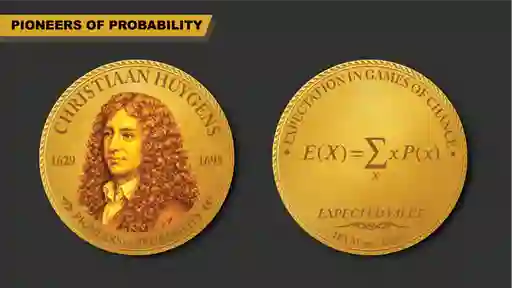

The answer he arrived at was the concept of expected value — one of the most important formulas in the history of decision-making under uncertainty. The expected value of a random outcome is the sum of each possible result, multiplied by the probability of that result occurring. E(X) = Σ x · P(x). That formula, which appears on the reverse of the IFA MarketCoin® for Huygens beneath the inscription "Expectation in Games of Chance" and "Expected Value," is the mathematical translation of a question every investor asks every day: what is a fair price for an outcome I cannot predict with certainty?

Before Huygens, this question had no rigorous answer. Gamblers used intuition. Merchants used rule of thumb. Insurance underwriters used experience. Huygens provided the formula that helped replace those approaches with a calculation. A fair price for an uncertain prospect is its expected value — the probability-weighted average of all possible outcomes. Nothing less may be rational to accept; nothing more is rational to pay.

◆ The Proof

In 1657, Huygens published De Ratiociniis in Ludo Aleae — On Reasoning in Games of Chance. It was the first printed textbook on probability ever written. Its importance to the history of probability cannot be overstated. Pascal and Fermat had solved the problem, but their letters were private. Without publication, ideas don't spread; without spread, there is no field. Huygens was the person who put the mathematics into print — and in doing so, gave a generation of mathematicians something to read, teach, and build upon. Jacob Bernoulli, who would extend probability theory in the next generation, annotated Huygens's text extensively. The De Ratiociniis was the primary text from which probability theory was learned for the next half-century.

In 1657, Huygens published De Ratiociniis in Ludo Aleae — On Reasoning in Games of Chance. It was the first printed textbook on probability ever written. Its importance to the history of probability cannot be overstated. Pascal and Fermat had solved the problem, but their letters were private. Without publication, ideas don't spread; without spread, there is no field. Huygens was the person who put the mathematics into print — and in doing so, gave a generation of mathematicians something to read, teach, and build upon. Jacob Bernoulli, who would extend probability theory in the next generation, annotated Huygens's text extensively. The De Ratiociniis was the primary text from which probability theory was learned for the next half-century.

The book is built on a foundational axiom that Huygens stated precisely: a fair game is one in which each player's expected gain equals zero. That is the definition of a fair bet. Nothing is owed to the house; nothing is extracted from the player. The expected value of the game, under fair conditions, is exactly the price of entry. This single axiom, rigorously applied across the book's propositions, generates the entire framework for evaluating uncertain prospects. It is a foundational benchmark used in evaluating investment performance. When a portfolio manager claims to generate alpha, they mean returns above what a fair, risk-adjusted bet would deliver. That benchmark begins with Huygens.

What made Huygens's formulation distinctive was his insistence on generality. He wasn't solving specific dice problems. He was establishing a general principle: that expectation is the right concept for valuing any uncertain outcome, and that it can always be calculated from first principles, regardless of the specific game, the number of players, or the structure of the payoffs. This generality is what made the formula portable — applicable far beyond the gambling table that had motivated it.

◆ The Legacy

The speed with which Huygens moved from hearing about the Pascal-Fermat correspondence to producing the first probability textbook — within about two years — says something important about the state of the field. The ideas were ready to be organized. What was missing was someone with the training, the time, and the rigor to write them down systematically. Huygens provided all three.

His contributions to probability were, however, a small fraction of his scientific output. In the same period he was writing the De Ratiociniis, he was also: discovering Titan, Saturn's largest moon, using a telescope he had ground himself; working out the true shape of Saturn's rings, which earlier observers had described as a pair of attached spheres; inventing the pendulum clock in 1656, which reduced timekeeping error from minutes per day to seconds per day and transformed navigation, astronomy, and commerce; developing the wave theory of light that would eventually displace Newton's particle theory; and deriving the formula for centrifugal force. He published major treatises on mechanics, optics, and horology. He became a founding member of the French Académie des Sciences in 1666 and lived in Paris under the patronage of Louis XIV until 1681, when deteriorating health drove him back to The Hague.

Huygens is, in some ways, the forgotten great scientist of the seventeenth century — overshadowed by Newton, whom he corresponded with and influenced; by Leibniz, whom he mentored in Paris; and by Descartes, his father's friend and philosophical predecessor. His portrait appeared on the Dutch twenty-five guilder banknote for decades. That quiet acknowledgment seems appropriate for a man who did extraordinary things without much seeking celebrity for doing them.

◆ Your Money

The expected value formula Huygens formalized is, at its core, the argument for passive investing stated in mathematical terms.

In a market where prices reflect available information efficiently, the expected return of any individual security is its fair value — the probability-weighted average of its future cash flows, discounted to the present. Under those conditions, trying to identify which securities will return more than their expected value is, by definition, a zero-sum game before costs. After costs, the average active manager will generally earn less than the market return, because active managers collectively are the market, and they are paying more to be in it.

The index fund investor accepts this logic and acts on it: rather than betting that one security's actual return will exceed its expected value, the index investor holds all securities in proportion to their market weight, capturing the aggregate expected return of the market as a whole. No single bet needs to be correct. The expected value of the whole portfolio is the expected value of the market.

Huygens didn't design this strategy. He was writing about dice in a Dutch city in 1657. But the principle — that the rational price for an uncertain outcome is its expected value, and that deviating from expected value requires evidence of an edge you don't have — is as direct a statement of the case for indexing as anything written in the three centuries since.

There is something fitting about the fact that the first printed textbook on probability — the book from which the next generation of mathematicians learned the subject — was written by a man who was primarily a clockmaker. Huygens spent his career measuring time with extraordinary precision. He also, in a book he wrote in his twenties almost as an intellectual exercise, gave us the formula for measuring something far harder to pin down: the fair price of what comes next.

Sources: Huygens, C. (1657). De ratiociniis in ludo aleae. In F. van Schooten, Exercitationum mathematicarum. Elsevier. Hacking, I. (1975). The emergence of probability. Cambridge University Press.

Disclosure: This article is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Any historical return examples referenced are hypothetical illustrations based on published index data and are not reflective of actual investor experience.

About the pen name: "Claude Hebner" represents a collaboration between Mark Hebner, founder and CEO of Index Fund Advisors, Inc., and Claude, Anthropic's AI. The research, historical narrative, and investment analysis in each article are the result of that partnership — human editorial judgment and decades of financial expertise combined with AI-assisted research and drafting.

X

X