There is a number buried in your investment account that no one has ever shown you: the return it must earn before you make a single cent. The more the account is traded, the higher that number climbs, and someone profits every time it does. In its fraudulent extreme it has a name, portfolio churning; the quieter, legal version sits in accounts that look perfectly respectable, very possibly including your own.

That extreme just landed in the regulatory record. This week, FINRA expelled the firm responsible and barred its two cofounders. One client account had been traded so heavily it would have needed to return more than 111% in a year just to cover what the trading was costing. Almost no portfolio in history has returned that in a year. In this case, losses were so significant that the investor had little opportunity to recover.

A statement full of trades reads like diligence — proof that someone is watching your money. In cost terms, it is the opposite. Movement is not always service. It cais often a charge. And most investors don't know their own number.

The Account That Had to Return 111% Just to Break Even

The number behind the headline is called the cost-to-equity ratio, and it's simpler than it sounds. It represents the return an account has to earn to cover what the trading costs — commissions, fees, all of it — before the investor is up a single dollar. FINRA found that in this case it had been pushed to a level that made achieving a profit highly unlikely.

The worst account would have needed to clear more than 111% in a year to break even. It was not alone. A second carried a cost-to-equity ratio above 69% and lost more than $345,000. A third sat above 67% and lost nearly $400,000. Across 20 customer accounts traded this way over nearly six years, the firm extracted roughly $2 million in commissions and trading costs while customers absorbed about $2.7 million in losses. The settlement was accepted without the firm admitting or denying FINRA's findings.

The people on the other end were not naive. The firm focused on high-net-worth investors reached through cold calling, used margin freely, and recommended the same trades across clients regardless of their circumstances.

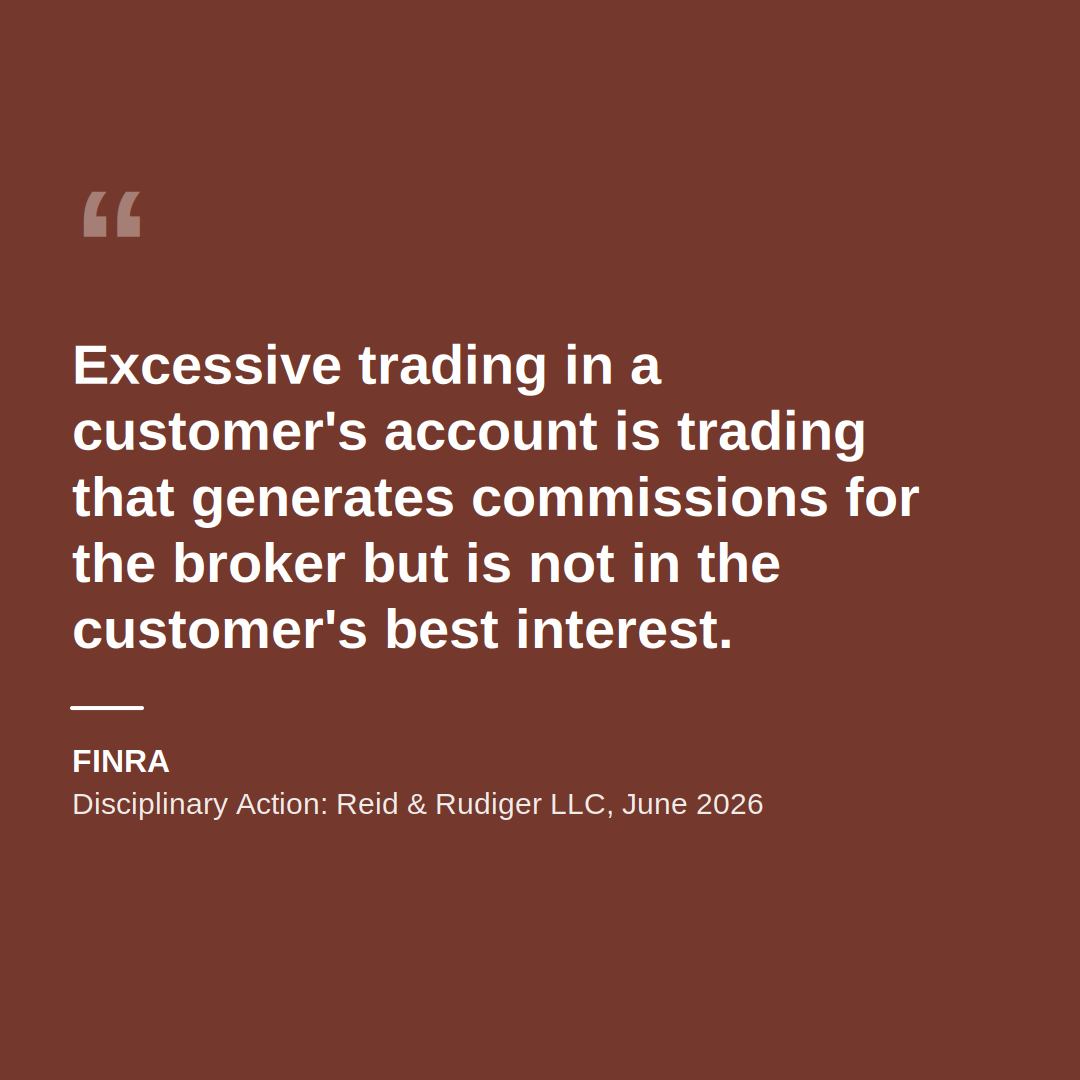

Two terms are worth getting straight, because the rest depends on them. FINRA defines excessive trading as trading that runs up commissions for the broker without serving the customer. Churning is that same excessive trading carried out with intent to defraud, or with reckless disregard for the client. One is a pattern. The other is a crime. The violations here ran from the Care Obligation of Regulation Best Interest to FINRA's own rules.

Why Every Account Has a Breakeven Cost

What makes this case useful is not how unusual it is, but how ordinary the mechanism behind it is. The firm sat at the far end of a spectrum that every account occupies. All trading carries a cost, and the more an account is traded, the higher the return it has to earn before the investor comes out ahead. Churning is the rule-breaking end of that spectrum. The same cost sits, legally and quietly, in any high-turnover account.

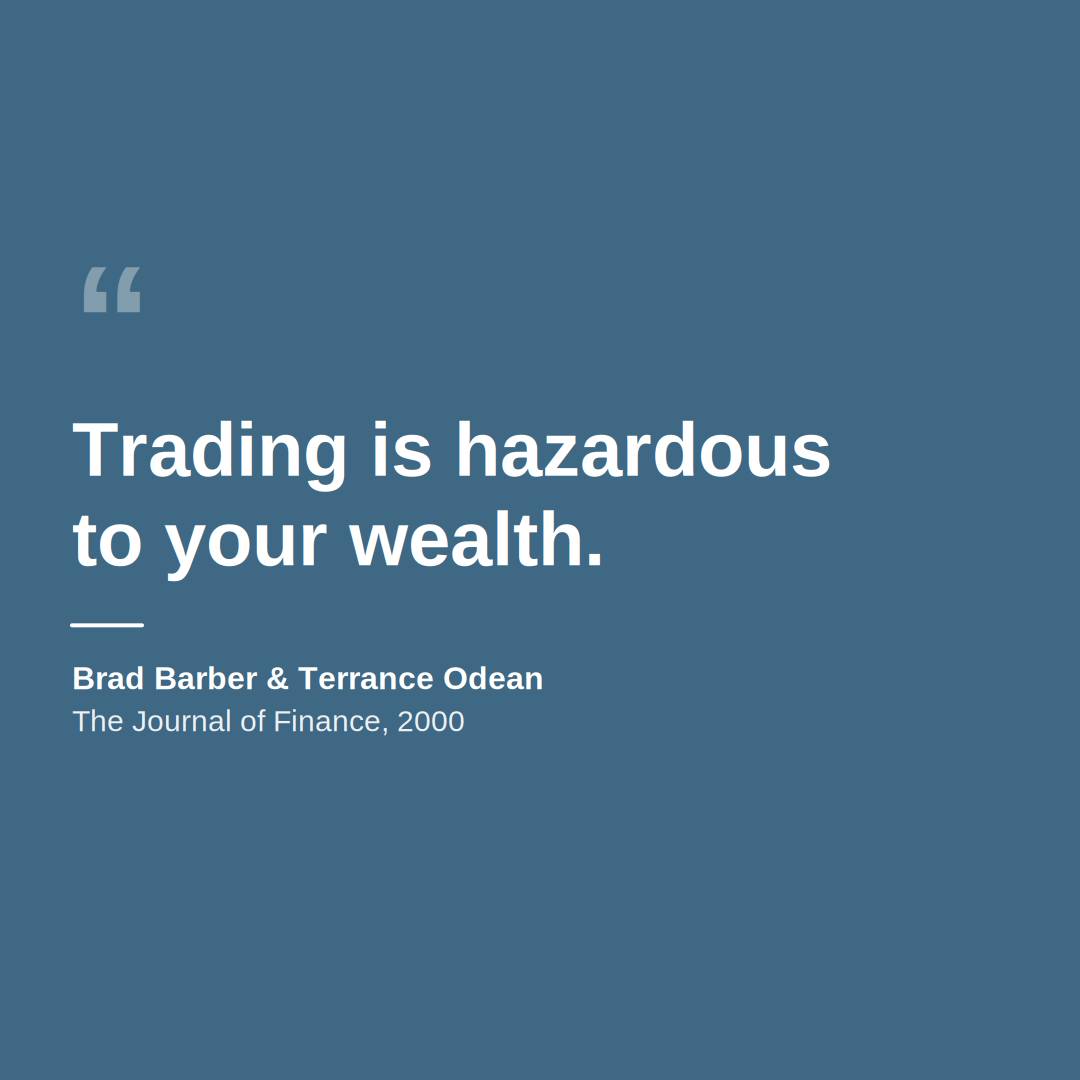

The everyday version has been measured. In a landmark study of 66,465 households at a large discount brokerage between 1991 and 1996, Brad Barber and Terrance Odean found that the most active traders earned 11.4% a year after costs while the market returned 17.9%. The average household earned 16.4% and turned over 75% of its portfolio annually. The gross returns of the busy and the patient were similar. The gap was costs. Their conclusion has become one of the most quoted lines in finance: "trading is hazardous to your wealth." These are historical averages, not a law of nature, but the tendency is strong, though outcomes can vary.

Turnover is a significant contributor to cost. Securities law has long leaned on a rough rule of thumb to read it: an annual turnover rate of two is an indication of excessive trading, four raises a presumption, and six a strong one. By that measure, even the least-traded of the expelled firm's accounts — an annualized turnover of about 6.92, with the range across accounts reaching 17.33 — had cleared the strongest line before you got anywhere near the worst ones (Investment Executive, 2026, citing FINRA's order).

So the question is never whether there was trading. Some turnover is right and necessary: rebalancing, harvesting a tax loss, trimming a position that has grown too large. The real question is whether the trading was worth its cost, and whether anyone bothered to check.

Paid for Activity, Not Outcomes

Why is anyone's cost higher than it has to be? The honest answer has two halves, and only one of them is what you would expect. When a firm is paid for transactions or for the assets it gathers, its interests may not always align with the client's.

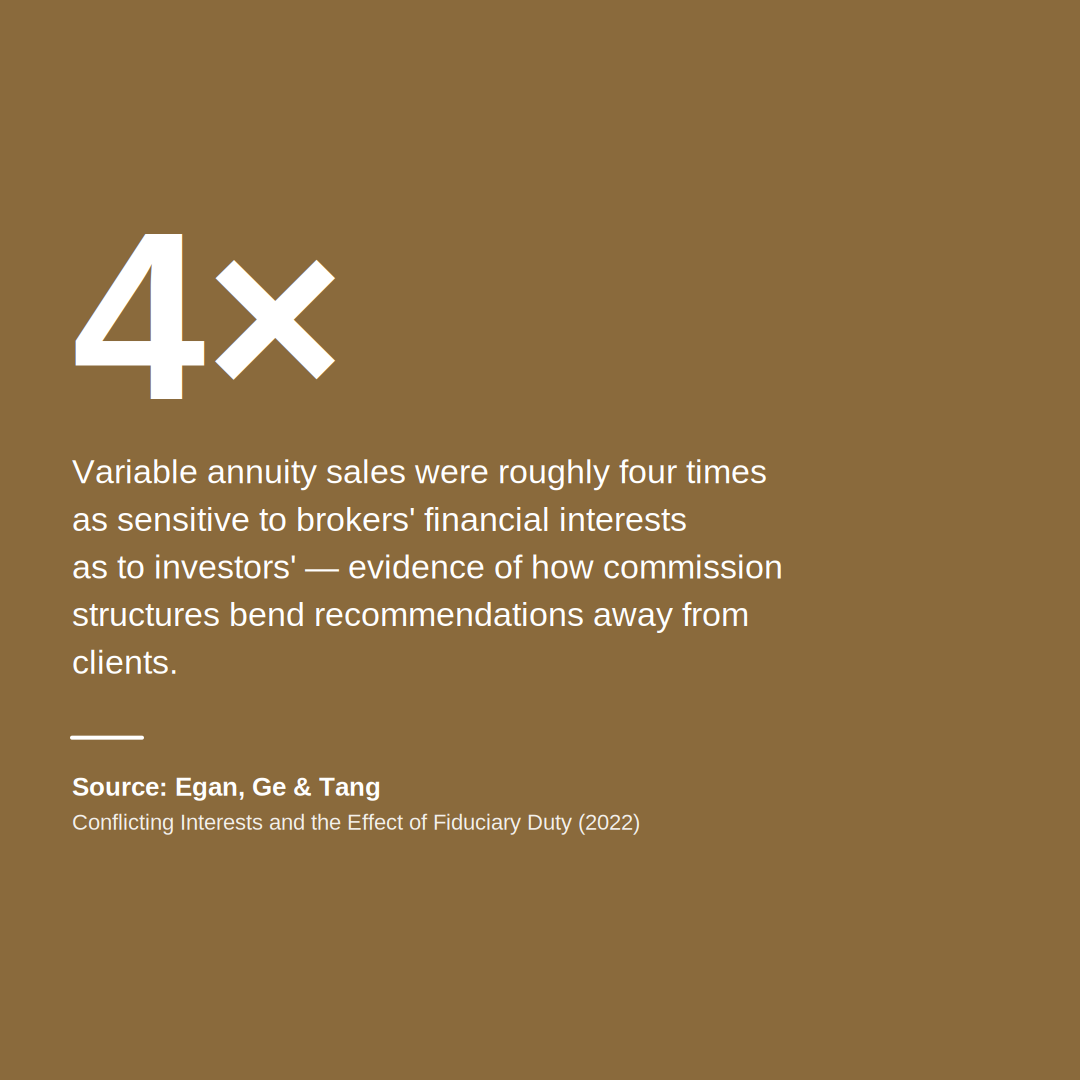

The cleanest evidence of how far they can pull comes from variable annuities. Mark Egan, Shan Ge, and Johnny Tang found that sales were "roughly four times as sensitive to brokers' financial interests as to investors'." When the Department of Labor proposed a fiduciary rule in 2016 (later struck down in court), sales of the highest-expense annuities — the ones that paid brokers most — fell by 52%. The product had not changed. The incentive had. The median commission on these annuities ran around 7% of the premium.

That is the cynical half. The other half is more uncomfortable, because it complicates the villain story. Studying a large group of advisors and their own money, Juhani Linnainmaa, Brian Melzer, and Alessandro Previtero found that advisors "typically invest personally just as they advise their clients": they trade frequently, chase returns, and favor expensive active funds. Their own net returns ran about minus 3% a year, in line with their clients'. And they kept at it after leaving the industry, when no commission was on the line. Some of the outcomes observed may reflect sincerely held beliefs rather than intentional misconduct.

Greed and conviction can, in some cases, lead to similar outcomes. Whether the cost is high because someone profits from it or because someone genuinely thinks the activity is the job, an investor's return may be affected in similar ways — which is exactly why structure matters more than character.

Reverse Churning: When Doing Nothing Costs You Too

The obvious fix is to move to a fee-based account. It helps. But the same incentive doesn't disappear — it inverts. Instead of an account traded to death, you may get an account nobody touches, billed a full advisory fee year after year for management that isn't happening. The trade-churned account and the untouched-but-billed account grow from one root: payment that rewards the arrangement rather than the advice.

This is reverse churning: charging an ongoing fee while doing little or no work. And it targets the very investor most likely to assume they are safe — the wealthy, buy-and-hold client in a wrap account, who has done everything right and figures a flat percentage protects them.

It also exposes a distinction the industry tends to blur. "Fee-based" is not "fee-only." In a working paper on dual-registered advisors — brokers and fiduciaries at the same time — Nicole Boyson found they charge an average of about 2.1% of assets under management, against roughly 1% at independent registered investment advisers, while routing clients into institutional share classes of the same underperforming funds. Many of them, she wrote, "appear to fall short of the fiduciary standard."

What Actually Brings the Cost Down

Here is the good news: some of these issues may be addressed with appropriate changes. Bringing the cost down comes down to two things you can control.

The first is the cost itself. Less turnover, lower total expense. Remember the most important finding from Barber and Odean: the gross returns of the active and the patient were roughly the same, and the difference was what trading took out. While returns are uncertain, investors may have more control over costs and fees.

The second is how your advisor is paid. In his book Index Funds: The 12-Step Recovery Program for Active Investors, IFA founder Mark Hebner sets the bar: a registered investment adviser, he writes, "is paid solely for advice, accepting no compensation for any investment products or trading recommended to clients." Pay someone that way, and it may reduce certain incentives to increase costs. It is the structure that does the work, not the person's good intentions — which is why behavior shifted the moment a best-interest standard merely loomed over variable annuities, and sales of the costliest products fell by 52%. Changes in incentives may influence behavior.

How to Read Your Own Statement

You do not need a forensic accountant to find your own number. You need three figures and one straight answer.

First, ask for your account's annual turnover rate: how much of the portfolio is bought and sold in a year. Second, ask for your all-in annual cost, every fee included — the everyday version of that cost-to-equity ratio. Third, ask precisely how your advisor is paid. Then the straight answer: whether they act as a fiduciary at all times and on all accounts , not just on some of them?

Watch for two opposite warning signs, and treat them as the same flag. One is a statement crowded with trades you did not request and cannot explain. The other is a static account, barely touched from one year to the next, still charged a full advisory fee every year. Both may indicate you are paying for something other than advice. And if any of these numbers turn out to be hard to get, that reluctance is itself an answer.

The Number Worth Asking About

Portfolio churning makes the news because the numbers are grotesque. But the cost that sits underneath it — the return your account has to earn before you make anything — is not exotic, not illegal, and not rare. It is just quiet. Most of the time nobody runs it up on purpose. Whether the cause is a cold-calling operation, a commission that tilts a recommendation, or an advisor who sincerely believes activity is the job, the number on your end behaves the same way.

What changes the picture is knowing the number exists and asking for yours. The firms that profit from a high cost depend on one thing: that you never think to ask what return your account has to earn before you are actually ahead. So ask it. Understanding this number may help investors make more informed decisions. That is the number worth asking about.

Resources

Barber, B. M., & Odean, T. (2000). Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance, 55(2), 773–806.

Boyson, N. M. (2019). The worst of both worlds? Dual-registered investment advisers [Working paper]. SSRN.

Egan, M., Ge, S., & Tang, J. (2022). Conflicting interests and the effect of fiduciary duty: Evidence from variable annuities. The Review of Financial Studies, 35(12), 5334–5386.

Linnainmaa, J. T., Melzer, B. T., & Previtero, A. (2021). The misguided beliefs of financial advisors. The Journal of Finance, 76(2), 587–621.

ROBIN POWELL is the Creative Director at Index Fund Advisors (IFA). He is also a financial journalist and the Editor of The Evidence-Based Investor. This article reflects IFA's investment philosophy and is intended for informational purposes only.

DISCLOSURES:

This article is for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. This material includes general educational information and should not be interpreted as individualized investment advice or a recommendation to take any specific action. Past performance is not indicative of future results. All examples and data cited are based on historical analysis and may not reflect future market conditions. Investing involves risks, including the possiblity of loss and principal. The mathmatical principles discussed illustrate theoretical concepts and should not be interprested as guarantees of investment outcomes. Diversivication does not ensure profit or protect against loss.

Any discussion of regulatory actions is based on publicly available information and should not be interpreted as representative of industry-wide practices. There is no guarantee that reducing turnover or fees will result in improved investment outcomes.

The information discussed is general in nature and may not be suitable for all investors. Examples and studies cited reflect specific time periods and may not be representative of all market conditions or investor experiences. Individual circumstances vary, and readers should consult a qualified professional regarding their personal situation. Index Fund Advisors, Inc. (IFA) believes the information to be accurate but does not guarantee its completeness or accuracy. This article was sourced and prepared with the assistance of artificial intelligence (AI) technology.For more information about Index Fund Advisors, Inc, please review our brochure at https://www.adviserinfo.sec.gov/ or visit www.ifa.com.

X

X