Pioneers of Probability · Episode 3

This video is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. The historical and mathematical concepts discussed are intended to illustrate the development of probability theory and its relevance to investing. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. The examples provided are hypothetical and based on historical index data, not an actual investment. Index returns do not reflect the performance of any actual portfolio or the deduction of advisory fees. Content is AI assisted.

◆ The Question

By 1620, Galileo Galilei had already done more for human knowledge than most scientists accomplish in several lifetimes. He had built telescopes of unprecedented power and turned them on the sky. He had observed the four largest moons of Jupiter — naming them the "Medicean Stars" in a shrewdly political gesture toward his patron Cosimo II de' Medici, Grand Duke of Tuscany — and used their orbits to argue that not everything in the heavens revolves around Earth. He had documented sunspots, mapped the rugged surface of the Moon, articulated the principle of inertia decades before Newton would formalize it, and established the law of free fall through painstaking experiment. Albert Einstein would later call him "the father of modern science." Stephen Hawking said he bears more responsibility for the birth of modern science than anyone else.

And yet one of the most conceptually elegant things Galileo ever did was solve a puzzle about dice for a group of courtiers who couldn't understand why their favorite bet kept winning.

It is easy to read this as a footnote — a minor diversion by a great mind between cosmological battles. But the dice problem, and the method Galileo brought to it, reveal something essential about what made him great. He applied to a small problem the same disciplinary force he applied to the motion of planets: replace intuition with measurement. Stop assuming. Count.

The puzzle had been nagging at the Medici court for years. When three dice are thrown and the results added, a total of ten appears more often than a total of nine. The frustrating thing — the thing that made it a genuine intellectual puzzle — was that both totals can be formed from exactly six distinct combinations of three numbers. Nine and ten looked mathematically identical. And yet experience said they weren't. The gamblers were right. The mathematics seemed to be wrong. They brought the question to Galileo, who was serving as Chief Mathematician and Philosopher to the Grand Duke of Tuscany, a position he had actively courted by naming Jupiter's moons after the Medici family and sending Cosimo a fine telescope. When the court had a hard problem, Galileo was the man they called.

◆ The Insight

Galileo's answer to the dice puzzle was not complicated. But it required a clarity of thinking that almost nobody had brought to the problem before him. The key distinction — the one that separates his analysis from all the intuitive reasoning that preceded it — was between combinations and permutations.

Galileo's answer to the dice puzzle was not complicated. But it required a clarity of thinking that almost nobody had brought to the problem before him. The key distinction — the one that separates his analysis from all the intuitive reasoning that preceded it — was between combinations and permutations.

A combination is a unique set of numbers: 1, 3, 5 is a combination that sums to nine. A permutation is a specific arrangement of those numbers across three distinct physical dice: die one shows 1, die two shows 3, die three shows 5. That is one permutation. Die one shows 3, die two shows 1, die three shows 5. That is a different permutation of the same combination. The courtiers had been counting combinations. They needed to count permutations.

When the courtiers counted six combinations for each of nine and ten, they were counting correctly. The error was treating each combination as a single outcome. A combination like 1-2-6, where all three numbers differ, can be arranged across three dice in six different ways. A combination like 1-4-4, where one number repeats, can only be arranged in three ways. And 3-3-3 can only be arranged one way. The dice are physically distinct objects. Every arrangement is a separate outcome.

This philosophical stance — that the book of nature is written in the language of mathematics, a phrase Galileo used explicitly in his later work The Assayer — is what connects the telescope and the dice table. In both cases, he was insisting that appearances can deceive, that intuition is unreliable, and that only careful, exhaustive measurement reveals the truth. He spent his career being persecuted for applying this principle to cosmology. In the dice problem, he applied it to a much smaller stage, with much lower stakes, and demonstrated its power in a form even a courtier could understand.

◆ The Proof

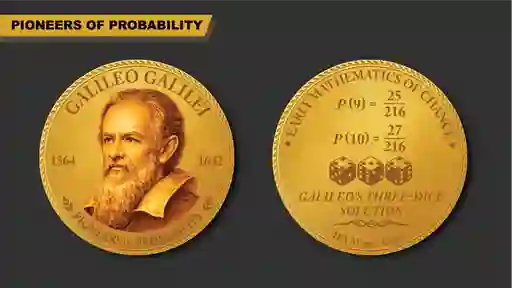

Three dice produce 216 possible outcomes — 6 × 6 × 6 — each one equally likely. Galileo counted all of them. When you add up the permutations of each combination that sums to nine, you get 25. When you count the same for ten, you get 27. The IFA MarketCoin® for Galileo records this directly on its reverse, beneath the inscription "Early Mathematics of Chance" and "Galileo's Three-Dice Solution": P(9) = 25/216, P(10) = 27/216.

A gap of two chances out of 216 — less than one percent. Invisible in a single session at the table. Clearly visible over thousands of throws. The gamblers had been right. The intuitive mathematics had been wrong. And the lesson embedded in that gap is one of the most important in the history of quantitative reasoning: what feels equal is not always actually equal, and only exhaustive enumeration can tell you the difference.

Galileo wrote up his analysis in a short essay known today as Sopra le Scoperte dei Dadi — On the Discoveries of Dice. It was never published in his lifetime. The manuscript circulated privately within the Medici court and was only printed decades after his death, when it appeared in his collected works. This matters for context: by the time Galileo was working on dice, he was already under pressure from the Church. The Roman Inquisition had investigated his views on heliocentrism in 1615. He was protected by the Medici connection but aware that his position was precarious. The Sopra le Scoperte dei Dadi was a service to the court, not a contribution to any mathematical project he cared deeply about. And yet it shows the same mind at work that was revolutionizing astronomy and physics — the insistence that problems be solved by systematic enumeration rather than intuitive reasoning, the willingness to do painstaking combinatorial counting rather than assume, and the clarity of exposition that made complex results immediately comprehensible.

◆ The Legacy

Galileo spent the last nine years of his life under house arrest at his villa in Arcetri near Florence, condemned by the Inquisition in 1633 for defending a picture of the cosmos that turned out to be correct. The Catholic Church formally acknowledged its error in 1992, when Pope John Paul II admitted that the Inquisition had been wrong. It had taken 359 years.

His dice essay, meanwhile, outlasted the Inquisition by considerably more. Within forty years of its private circulation, Pascal and Fermat built the formal theory of probability that Galileo's counting method had anticipated. They gave it formulas, notation, and generality. But the philosophical core — insisting on exhaustive enumeration over intuitive reasoning, demanding that every possible outcome be counted before any conclusion be drawn — was already present in a few pages about dice, written in the margins of a court astronomer's responsibilities, and never intended for publication.

Galileo proved that the gap between intuition and reality is real, measurable, and consequential. The next question was whether mathematics could do more than count — whether it could predict. That question fell to two men exchanging letters in the summer of 1654.

◆ Your Money

The gap between intuition and reality that Galileo identified at the dice table is one of the most expensive cognitive errors in modern finance.

Morningstar's annual Mind the Gap study tracks the difference between what mutual funds return and what investors in those funds actually earn. The gap arises from behavior — specifically, from the same pattern Galileo identified: people act on intuition rather than on what the numbers actually show. They see a fund that has risen and buy it, because their instinct says momentum will continue. They see a fund that has fallen and sell it, because their instinct says the losses will compound. Over the decade ending in 2024, this intuition-driven behavior cost the average investor approximately 1.2 percentage points per year relative to a simple buy-and-hold approach — with investors capturing roughly 85 percent of what patient inaction would have delivered.

One point two percent (1.2%) doesn't sound large. Compounded over ten years, it is the difference between capturing the market's full return and giving away fifteen percent of it. Compounded over a working lifetime, it is the difference between a comfortable retirement and a constrained one.

The courtiers of Florence thought they understood the odds because the combinations looked equal. They were wrong, and only Galileo's counting proved it. Today's investors think they understand the market because they follow it closely and act on what they see. They are making the same category of error — trusting the appearance of patterns over the evidence of measurement. A century of behavioral finance data supports what Galileo established at a much smaller scale: instinct, applied to probabilistic systems, is systematically and expensively wrong.

Three dice, 216 outcomes, a two-in-216 gap, and a lesson that has not changed in four centuries. If you want to know the odds, measure. Everything else is a hunch.

Sources: Galilei, G. (c. 1620). Sopra le scoperte dei dadi. In Opere di Galileo Galilei (Vol. 8, pp. 591–594). Barbera. Ptak, J. (2025). Mind the gap: A report on investor returns in the United States. Morningstar. Wootton, D. (2010). Galileo: Watcher of the skies. Yale University Press.

Disclosure: This article is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Any historical return examples referenced are hypothetical illustrations based on published index data and are not reflective of actual investor experience

Content is AI-assisted. Index Fund Advisors, Inc. is a registered investment adviser. For additional information, please visit adviserinfo.sec.gov or www.ifa.com.About the pen name: "Claude Hebner" represents a collaboration between Mark Hebner, founder and CEO of Index Fund Advisors, Inc., and Claude, Anthropic's AI. The research, historical narrative, and investment analysis in each article are the result of that partnership — human editorial judgment and decades of financial expertise combined with AI-assisted research and drafting.

X

X