Pioneers of Probability · Episode 4

This video is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. The historical and mathematical concepts discussed are intended to illustrate the development of probability theory and its relevance to investing. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. The examples provided are hypothetical and based on historical index data, not an actual investment. Index returns do not reflect the performance of any actual portfolio or the deduction of advisory fees. Content is AI assisted.

◆ The Question

Pierre de Fermat held the title of King's Counselor at the Parlement of Toulouse. He was a magistrate, a trained jurist, a man of solid provincial standing who administered law, presided over criminal cases, and carried the routine weight of public office. He was fluent in six languages — French, Latin, Occitan, classical Greek, Italian, and Spanish — and by contemporary accounts was an accomplished poet in several of them. He had a wife, Louise de Long, five children, and a comfortable house in the south of France.

Mathematics was his hobby.

That sentence understates the situation so dramatically it becomes comic. Fermat was not a hobbyist mathematician in the way that a person is a hobbyist woodworker or gardener. He was, in the considered judgment of his contemporaries and of historians across four centuries, one of the two or three greatest mathematical minds of the seventeenth century — ranking alongside Descartes and Newton. He co-invented analytic geometry independently of Descartes, anticipated the differential calculus that Newton and Leibniz would later formalize, revolutionized the theory of numbers, made foundational contributions to optics, and co-founded the mathematical theory of probability. He did all of this in the margins of his judicial career, in letters to correspondents, almost entirely without publishing a word.

He was so reluctant to publish that he became notorious for it. He would announce results in correspondence — daring his correspondents to prove them, often providing no proof himself, sometimes scribbling theorems in the margins of books. His most famous marginal note, written in a copy of Diophantus's Arithmetica, claimed he had a "marvelous proof" of what became known as Fermat's Last Theorem. That proof, if it ever existed, was never found. The theorem itself went unproven for 358 years, until Andrew Wiles finally cracked it in 1994 using mathematical tools that didn't exist in Fermat's century. The margin, as Fermat noted, was too narrow to contain his alleged proof — and for three and a half centuries, that might as well have been the wittiest joke in mathematics.

◆ The Insight

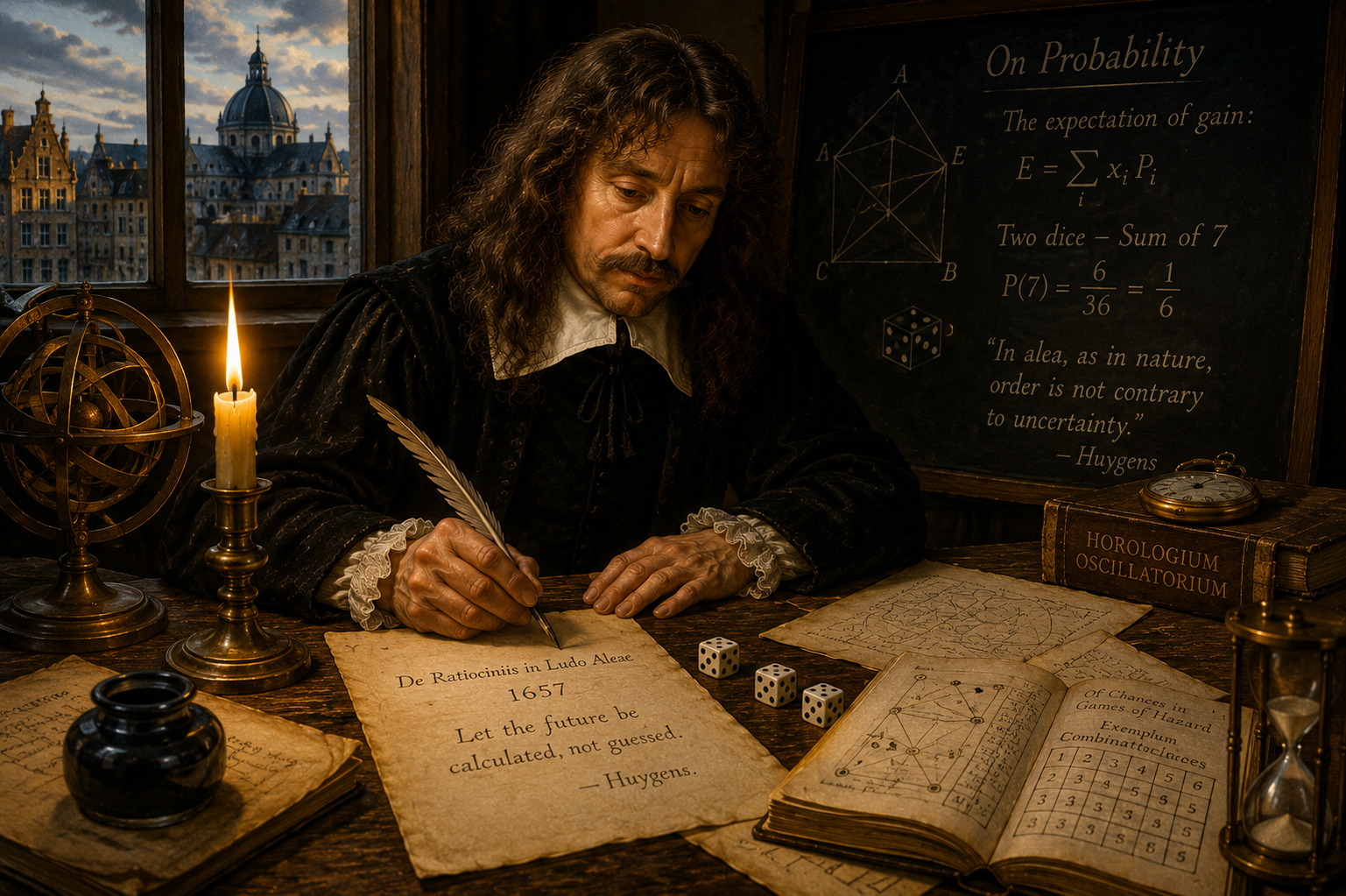

In the summer of 1654, a letter arrived in Toulouse from Paris. It came from Blaise Pascal, a man twenty-two years Fermat's junior who was already famous for building the first mechanical calculator at nineteen and for his brilliant work in geometry and physics. Pascal had been approached by a gambler named Antoine Gombaud, the Chevalier de Méré, with a question that had been vexing game-players for two centuries: the Problem of Points.

In the summer of 1654, a letter arrived in Toulouse from Paris. It came from Blaise Pascal, a man twenty-two years Fermat's junior who was already famous for building the first mechanical calculator at nineteen and for his brilliant work in geometry and physics. Pascal had been approached by a gambler named Antoine Gombaud, the Chevalier de Méré, with a question that had been vexing game-players for two centuries: the Problem of Points.

The problem is this. Two players are gambling. The game is fair — each has an equal chance of winning each round. They agree to play until one of them wins a fixed number of rounds. Then, for whatever reason, they must stop before the game is finished. How should the pot be divided?

Existing solutions, including one proposed by the Renaissance mathematician Luca Pacioli in 1494, divided the stakes based on what had already happened — rounds played, points scored, current lead. This approach seems intuitive. It is mathematically wrong. The crucial insight that everyone before Fermat had missed was that the fair division depends not on what has happened but on what was about to happen. The pot should be divided according to each player's probability of winning from this exact point forward. The past is context. The future is what you're buying.

Fermat understood this instantly. And he knew exactly how to calculate it.

◆ The Proof

Fermat's method was exhaustive enumeration: imagine every possible future sequence of the game, count the paths in which each player wins, and divide the pot in that proportion. If player A needs r more wins and player B needs s more wins, then the game will end in at most r s − 1 more rounds. Fermat systematically counted every possible combination of outcomes across those rounds, determined who would win each scenario, and summed the results.

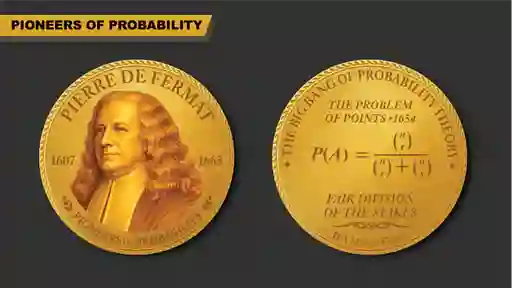

The IFA MarketCoin® for Fermat honors this approach on its reverse, beneath the inscription "The Big Bang of Probability Theory" and "Fair Division of the Stakes." The coin shows a combinatorial formula — P(A) expressed as a ratio of combinations — capturing Fermat's key move: the probability of A winning is the number of future paths in which A prevails, divided by the total number of equally likely future paths. The Problem of Points, identified on the coin as the breakthrough of 1654, is labeled precisely because this correspondence with Pascal was the founding moment of mathematical probability as a formal discipline.

The five letters between Fermat and Pascal that summer are among the most consequential documents in the history of mathematics. The two men agreed on answers, disagreed on methods — Pascal used a recursive triangle, Fermat used direct enumeration — and the very fact that two such different approaches yielded identical results gave both of them confidence that they had found something real. They were not solving a puzzle about dice. They were discovering the mathematical structure of the future.

Fermat never published the solution. The letters circulated privately, copied and recopied by the network of Parisian intellectuals around Mersenne's correspondence circle. They were printed only after both men were dead. This was entirely typical of Fermat. He rarely published, never sought public credit, and seemed genuinely indifferent to establishing formal priority for results he knew he had found. He also nearly died in 1652, when the plague struck Toulouse with such force that a colleague incorrectly reported Fermat's death. He recovered. He had more problems to solve.

◆ The Legacy

Fermat was, by temperament, the polar opposite of the ambitious, publishing-driven scientist we imagine when we think of great discoverers. He worked alone, shared selectively, and left the burden of proof to others. Where he did correspond, it was often to pose challenges rather than to establish claims. He taunted the best mathematicians in England, France, and the Netherlands with number-theory problems that he said he had solved, providing no solutions, watching to see who could match him. Most could not.

What emerged from the Fermat-Pascal correspondence was not just a solution to a gambling problem. It was the first demonstration that the mathematics of uncertain outcomes could be placed on rigorous foundations — that probability was not a matter of intuition or experience, but a calculable, derivable property of any well-defined situation involving chance. Every bond price, every insurance premium, every risk model built since 1654 traces its logical ancestry back to those five letters.

His legacy in number theory alone — Fermat's Little Theorem, Fermat's Last Theorem, his work on perfect numbers and prime factorization — would be sufficient for a permanent place in mathematical history. That he co-founded probability theory on the side, as a hobby, between judicial appointments, is a biographical fact so improbable it seems invented.

◆ Your Money

The core insight Fermat contributed to probability theory — that you should divide the pot based on the future, not the past — has a direct and often uncomfortable parallel in how investors manage portfolios.

Most investment behavior is backward-looking. Investors buy funds that have risen recently, sell funds that have fallen, fire managers who underperformed last year, and hire managers who outperformed. All of this is reasoning from the past, exactly as Pacioli's flawed solution reasoned from the past. The mathematically correct approach — the one Fermat understood in 1654 — is to reason from the future: what is the probability distribution of outcomes from this point forward, given the current state of the game?

For a diversified index investor, that question has a principled answer: the expected future return of the market portfolio, compounded over time, has historically been positive. That is the point from which rational allocation begins. Not last year's returns. Not last month's headlines. The distribution of plausible futures, and the probability-weighted expected value of each. Fermat would have recognized the framework immediately. He invented it.

Sources: David, F. N. (1962). Games, gods and gambling. Charles Griffin. Devlin, K. (2008). The unfinished game. Basic Books. MacTutor History of Mathematics, University of St Andrews.

Disclosure: This article is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Any historical return examples referenced are hypothetical illustrations based on published index data and are not reflective of actual investor experience

Content is AI-assisted. Index Fund Advisors, Inc. is a registered investment adviser. For additional information, please visit adviserinfo.sec.gov or www.ifa.com.About the pen name: "Claude Hebner" represents a collaboration between Mark Hebner, founder and CEO of Index Fund Advisors, Inc., and Claude, Anthropic's AI. The research, historical narrative, and investment analysis in each article are the result of that partnership — human editorial judgment and decades of financial expertise combined with AI-assisted research and drafting.

X

X