From railroads to AI, many investment gold rush follows the same script: excitement builds, investors pile in, and many incur losses. The fear of missing out has been punishing investors for centuries. Here's what the evidence says about why it keeps happening, and what to do about it.

In 1849, around 300,000 people rushed to California chasing gold. Most came home broke. The people who built lasting fortunes? They sold the shovels. Levi Strauss made durable pants for miners. Henry Wells and William Fargo opened a bank to serve the prospectors and the booming economy around them. John Studebaker got rich manufacturing wheelbarrows. The gold-seekers did the backbreaking work. The suppliers collected the steady profits.

That pattern has repeated with many major technological booms since, from railroads to airlines to the internet. And with AI stocks surging and investor excitement running hot, it's playing out again.

The driving force is something investors now have a name for: FOMO, or the fear of missing out. A stock or sector soars. Friends and pundits can't stop talking about it. Staying on the sidelines starts to feel reckless. So you buy in, often after a big run up.

What FOMO actually does to investors

FOMO isn't just a feeling. It's a predictable behavior pattern with measurable financial consequences.

The concept predates the acronym. Marketing strategist Dan Herman identified the "fear of missing out" in consumer research in the mid-1990s. Patrick McGinnis coined the acronym in a 2004 article in The Harbus, Harvard Business School's student newspaper. But the behavior itself — watching others profit and feeling compelled to follow — has been driving bad investment decisions for centuries.

Larry Swedroe, author or co-author of 18 books on investing, describes the cycle bluntly: "Your friends are invested in high-tech stocks like Nvidia "Your friends are invested in high-tech stocks like Nvidia, or whatever's the latest meme stock they're touting on Reddit. The stocks run up and you're jealous. So you have this fear that you're going to miss out. But the people who do that end up buying after the stuff has already run up, and then when it goes down, their stomach takes over and yells 'get me out.' And they panic and sell."

Buy high. Sell low. Repeat.

In Index Funds: The 12-Step Recovery Program for Active Investors, IFA founder Mark Hebner traces this instinct to the earliest stock markets. He describes investors being "swept up in the allure of amassing quick fortunes" in 18th-century Amsterdam, where streets "erupted into a trading frenzy" as speculators scrambled to get rich from what was then called "the wind trade."

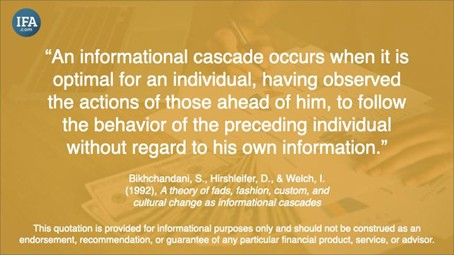

The academic explanation comes from Bikhchandani, Hirshleifer, and Welch. Their landmark 1992 paper on informational cascades showed how rational individuals end up making irrational collective decisions. Each person infers information from the actions of those ahead of them. Before long, the crowd is following the crowd, and nobody is following the evidence.

Financial media accelerates the problem. As Hebner puts it, "the financial news media and Wall Street feed the fear, anxiety, and other stressful emotions experienced by investors, resulting in less than favorable investment outcomes." Headlines don't just report FOMO. They manufacture it.

What research says about FOMO and returns

Studies on what researchers call "investment-specific FOMO" show it increases market participation, trading frequency, and the amounts people invest. Combined with overconfidence, recency bias, and loss aversion, FOMO may explain a substantial share of the variation in investment outcomes. The effects are strongest in volatile markets like cryptocurrency, and they're amplified by mobile technology that keeps the highlight reel of other people's gains in your pocket at all times. Younger, less experienced investors appear particularly exposed.

One caveat: most of these studies measure behavioral proxies — including how often people trade, how much risk they take, and how they time their entries and exits — rather than realized returns. But that's less reassuring than it sounds. The behaviors FOMO produces are the same ones decades of broader research have shown can erode wealth.

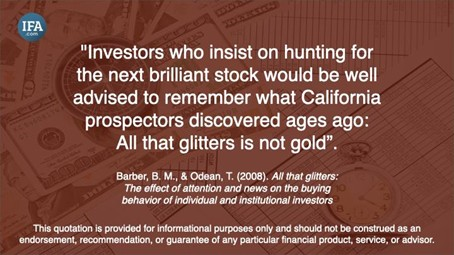

Barber and Odean's work puts numbers on it. Their 2000 study of more than 66,000 households found that the most active traders earned 11.4% annually while the market returned 17.9%. A follow-up 2008 study showed individual investors disproportionately buy "attention-grabbing" stocks: those making news, experiencing unusual trading volume, or posting extreme single-day moves. That's FOMO's fingerprint in the data, years before anyone used the term.

Swedroe sees the same dynamic play out constantly: "When you get this excitement, investor sentiment is high. That means the stocks have probably run up, and you're buying too high. And the stocks where the sentiment is poor, they've crashed and now valuations are lower." The crowd's enthusiasm, it turns out, can be a contrarian signal.

Why most technology revolutions punish stock pickers

Know your financial history. It's a great defense against FOMO. Most previous technological revolutions have punished investors who tried to pick the winners, even when they were right about the technology itself.

"The best thing is to know your financial history," Swedroe says. "We've gone through massive technological innovations before." The technology reshapes the world. The investors who bet on it often times lose money. Consumers and companies that use the new tools capture the gains, not the companies that build them.

Start with railroads. In the 1800s, England went through a massive railroad building boom. Investors poured money in. The majority got burned. The public benefited enormously from cheaper, faster transport.

Then airlines. "Airlines clearly changed the way we travel," Swedroe says. "And yet airlines have generally been a godawful investment." Travelers won. Shareholders didn't.

The dotcom era drove the point home more painfully. "Think about if you had decided that search engines were going to be the wave of the future," Swedroe says. "What would you have bought? Netscape. Not Google. Netscape was the dominant player." He rattles off the casualties. Amazon nearly went bankrupt. Blackberry dominated mobile and then got overtaken. Being right about the technology told you nothing about which stocks to own.

So who profited? Swedroe points to companies that used the internet as a tool rather than selling it as a product. "Think about how the internet enabled the Costcos and the Walmarts to improve their inventory and tracking and shipping, all these things that drive costs down," he says.

Gold rush, all over again. The picks-and-shovels sellers, the businesses that put new technology to work, built durable wealth. The speculators who rushed to stake claims mostly came up empty.

"We can't tell who the winners will be," Swedroe says. That's not a failure of analysis. It's how disruption works. The survivors become obvious only in hindsight, which is when it's too late.

Why AI stocks are the latest test of investor discipline

AI is genuinely transformative. Swedroe doesn't dispute that. "Clearly AI is a game changer," he says. But that's exactly why it's triggering the same FOMO dynamics that can punish.

"We don't know which industries will be affected, who will be the winners," Swedroe says. Take the most obvious candidate. "Nvidia looked like a great winner. Maybe it will continue to be, but maybe some startup will get ahead of them. We just don't know."

The uncertainty runs through the AI economy. Software companies that sell per-seat licenses could be in serious trouble if AI means fewer people are needed. But integrated systems that rely on proprietary databases? "AI is just going to make them even more important," Swedroe says. Good luck sorting one category from the other in advance.

He also raises a less discussed concern. Retail investors are increasingly using AI tools to make investment decisions. "They're all going to use the same tools, Claude or whatever, and that could lead to more of the FOMO, more chasing, and more volatility," he says. AI might not just be the thing investors are chasing. It might be amplifying the chase.

The Magnificent 7 stocks climbed roughly 76% in 2023. Many investors saw an invitation to pile in. But there's a more useful way to interpret extraordinary returns — one that explains what a 76% gain actually represents, and why it shouldn't change what you expect to happen next.

A smarter way to think about extraordinary returns

When a stock's price surges, its expected future return remains consistent with its risk. The next return is simply another draw from the same probability distribution — uncertain, as it always was.

This is counterintuitive, and it's the best intellectual weapon against FOMO. Companies raise money by issuing stocks and bonds. The return investors expect on those securities is the company's cost of capital: the rate needed to attract funding. An investor's expected return and the company's cost of capital are two sides of the same coin.

And every trade has another side: a seller willing to accept cash today in exchange for future returns. Prices move as buyers and sellers negotiate what rate of return each side demands. Stocks aren't objects you can pick from a tree — someone is always giving up future returns to get out.

The chart below puts that pattern into historical context. It tracks companies before and after they first entered the top ten largest US stocks by market cap over a 96-year period. In the three years before joining the top ten, those companies delivered excess returns averaging 27% a year above the market. In the ten years after joining, the excess return averaged –1.5%.

That's not evidence that the stocks collapsed. It's evidence that once a company becomes very large, the market has already priced in its prospects. Future returns tend to revert toward what the asset's risk actually justifies — which is market-like, not extraordinary. The next outcome is still uncertain. But the reasonable expectation is a return to normal, not another windfall.

Now apply that to the Magnificent 7, which returned roughly 76% in 2023. Does 76% look like a reasonable cost of equity for some of the most financially powerful companies on earth? These businesses can borrow at a fraction of that rate. If their actual cost of equity runs around 10%, then 76% was not a reasonable cost of capital. It was a windfall — a low-probability outcome from the tail of the distribution, not a new baseline. The expected return going forward remained around 10%, as it has been for growth stocks for 97 years.

A practical test follows. When an extraordinary return triggers that familiar FOMO pull, ask one question: "Does this look like a reasonable cost of capital for this company?" If the answer is no, the gap between what just happened and what you can reasonably expect isn't an opportunity. The most likely path forward is simply the asset's long-run expected return for its level of risk — not another windfall.

Why broad diversification is the real antidote

A diversified portfolio already owns some of whatever's going up. No need to pick champions, read tea leaves on Nvidia versus some unknown startup, or guess which software companies survive the AI shakeout. The exposure is already there.

"Whatever stock has gone up, the odds are you own some of it in one of your index or other funds," Swedroe says. That alone should take the edge off. But he goes further, arguing that genuine diversification extends beyond just owning the whole market.

"If I own a total stock market fund, there's really nothing wrong with that as a base case strategy," he says. "But that gives me only exposure to one factor," meaning market beta, the overall market return. Total market funds are cap-weighted: money concentrates in the biggest companies. Exposure to smaller and cheaper stocks is minimal, even though those categories have historically delivered higher expected returns.

Investors who want real diversification, Swedroe argues, need to tilt intentionally toward additional factors: independent sources of return like size (smaller companies), value (cheaper stocks), and profitability (companies with stronger earnings). The more independent return drivers in a portfolio, the less wealth depends on any single stock, sector, or trend. That said, factor tilts can underperform for long stretches. Past premiums don't guarantee future ones.

The objection people always raise: doesn't diversification mean missing the biggest winners? It does. But as the history of railroads, airlines, and dotcom stocks makes plain, it also means missing the biggest losers. Nobody can reliably tell them apart beforehand.

Swedroe's advice is blunt: "The best thing to do is stop reading all the headlines. Just have a widely diversified portfolio."

What to do now

FOMO is predictable, which means it's manageable. Five steps can help.

- Name it when you feel it. When a surging stock makes you itch to buy, recognize the pattern. The same impulse drove investors into railroad shares, dotcom stocks, and meme stocks. Knowing the history doesn't make the feeling disappear, but it weakens its grip.

- Ask the cost-of-capital question. Does this return look like a reasonable cost of equity for this company? If a stock delivered 76% in a year but the company can borrow at a fraction of that rate, that return was a low-probability tail outcome — not the new expectation. The expected return going forward is anchored to the company's cost of capital.

- Check your existing exposure. If you own a diversified portfolio, you likely already hold some of whatever's running. You're already in the game.

- Diversify your return drivers. Consider whether your portfolio relies on a single factor or draws on several sources of expected return. Size, value, and profitability premiums have historically rewarded patient investors, but they can take years to materialize. The commitment needs to be long-term.

- Cut the noise. Swedroe's advice bears repeating: stop reading the headlines. Financial media is designed to trigger the exact emotions that lead to bad decisions. A quieter information diet won't cost you returns. It may help you avoid emotional decisions.

Own the mountain

In 1849, the prospectors who chased California gold mostly came home with nothing. The people who built lasting wealth — Strauss, Wells, Fargo, and Studebaker — supplied the tools, served the growing economy, and played a longer game. They didn't bet on one claim. They positioned themselves to benefit no matter where the gold turned up.

Every technological revolution since has followed the same script. AI is following it now. The names change. The excitement feels new. The outcome rarely is.

You can stake everything on finding the next Nvidia before everyone else does. Or you can own the whole mountain — a portfolio built to capture returns from wherever they come — and let the prospectors chase their luck.

Resources

Barber, B. M., & Odean, T. (2000). Trading is hazardous to your wealth: The common stock investment performance of individual investors. The Journal of Finance, 55(2), 773-806.

Barber, B. M., & Odean, T. (2008). All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies, 21(2), 785-818.

Bikhchandani, S., Hirshleifer, D., & Welch, I. (1992). A theory of fads, fashion, custom, and cultural change as informational cascades. Journal of Political Economy, 100(5), 992-1026.

Hebner, M. T. (2025). Index funds: The 12-Step Recovery Program for Active Investors. IFA Publishing.

Image: California Gold Rush sailing card, circa 1849.

ROBIN POWELL is the Creative Director at Index Fund Advisors (IFA). He is also a financial journalist and the Editor of The Evidence-Based Investor. This article reflects IFA's investment philosophy and is intended for informational purposes only.

DISCLOSURES:

This article is for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. Past performance is not indicative of future results. All examples and data cited are based on historical analysis and may not reflect future market conditions. Investing involves risks, including the possible loss of principal. The mathematical principles discussed illustrate theoretical concepts and should not be interpreted as guarantees of investment outcomes. Diversification does not ensure a profit or protect against loss.

The information discussed is general in nature and may not be suitable for all investors. Individual circumstances vary, and readers should consult a qualified professional regarding their personal situation.

Index Fund Advisors, Inc. (IFA) believes the information to be accurate but does not guarantee its completeness or accuracy. This article was sourced and prepared with the assistance of artificial intelligence (AI) technology.

For more information about Index Fund Advisors, Inc, please review our brochure at https://www.adviserinfo.sec.gov/ or visit www.ifa.com.

X

X