Pioneers of Probability · Episode 7

This video is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. The historical and mathematical concepts discussed are intended to illustrate the development of probability theory and its relevance to investing. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. The examples provided are hypothetical and based on historical index data, not an actual investment. Index returns do not reflect the performance of any actual portfolio or the deduction of advisory fees. Content is AI assisted.

◆ The Question

Gottfried Wilhelm Leibniz has been called the last universal genius — a designation that, the more you learn about him, seems less like flattery and more like understatement. He was a philosopher of the first rank, a mathematician who co-invented calculus independently of Newton, a logician who anticipated modern formal logic by two centuries, a diplomat who negotiated peace treaties among warring European powers, a theologian who sought to reconcile Catholicism and Protestantism, a physicist who debated the nature of space and time with Newton's allies, a geologist who speculated on the formation of the Earth, a historian who catalogued the genealogy of the House of Brunswick, and an engineer who designed water pumps for the silver mines of the Harz Mountains. He also developed the binary number system — the 1s and 0s that every computer on Earth now runs on.

He did all of this while holding a day job. For most of his adult life, Leibniz served as a court official in Hanover — first as librarian, then as privy counselor and official historian, advising dukes, drafting correspondence, and managing the kind of administrative work that consumed most of his time and almost none of his imagination. The mathematics, the philosophy, the logic, the probability theory — all of it was done in the margins of a diplomatic career, in letters to correspondents across Europe, in manuscripts that were never published and were only rediscovered centuries after his death.

Leibniz was born in Leipzig in 1646, the son of a professor of moral philosophy who died when the boy was six. He taught himself Latin from his father's library before he was old enough to attend school, then taught himself Greek, then worked his way through the philosophy and theology of the classical world on his own. He completed a bachelor's degree in philosophy at fifteen and a doctorate in law at twenty, having been turned down for a degree at Leipzig because the faculty considered him too young. The University of Altdorf offered him a professorship immediately upon granting his doctorate. He declined, saying he had very different things in view.

◆ The Insight

Leibniz trained as a lawyer and spent decades navigating legal disputes, inheritance questions, and evidentiary problems as a professional advisor. This shaped his thinking about probability in a way that set him apart from every other thinker in this series.

The mathematicians who preceded him — Cardano, Galileo, Pascal, Fermat, Huygens, and Jacob Bernoulli — all built their probability theory on repeatable events: dice, cards, coin flips, gambling games. The mathematics they developed was fundamentally about frequencies — how often an outcome occurs across many trials. This is a powerful framework, and it underpins most of classical statistics. But it cannot answer a question that Leibniz, as a lawyer and logician, knew was equally important: how certain should a rational person be about a singular unrepeatable event?

You cannot run a murder trial a thousand times to observe the frequency of guilt. A disputed will, a contested inheritance, a witness whose testimony may or may not be credible — these situations happen once. The evidence is partial. The facts are uncertain. A judge must still reach a verdict. What is the rational basis for that verdict, and can it be given a mathematical structure?

Leibniz argued that it could. His key move was to reframe probability as a property of the mind rather than solely a property of the world. The die has six equally likely faces — that is a fact about the die. But the probability that a particular witness is telling the truth is not a fact about the witness in the same way. It is a measure of how confident a rational, well-informed person should be in that testimony, given all available evidence. Leibniz called these degrees of certainty — a continuous spectrum running from impossible at one end to certain at the other, with every claim a rational agent can make sitting somewhere along that line, its position shifting as new evidence arrives.

◆ The Proof

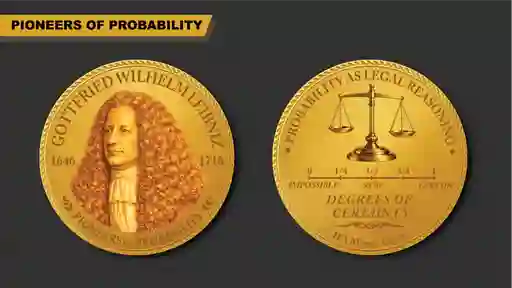

The IFA MarketCoin® for Leibniz captures this idea directly on its reverse. The coin shows a horizontal scale running from "Impossible" on the left through measured gradations — 1/4, 1/2, 3/4 — to "Certain" on the right, with scales of justice balanced above it, beneath the inscription "Probability as Legal Reasoning" and "Degrees of Certainty." This is not decorative. It is the philosophical core of Leibniz's contribution: probability as a language for measuring rational belief, applicable wherever decisions must be made under uncertainty, not just in games of chance.

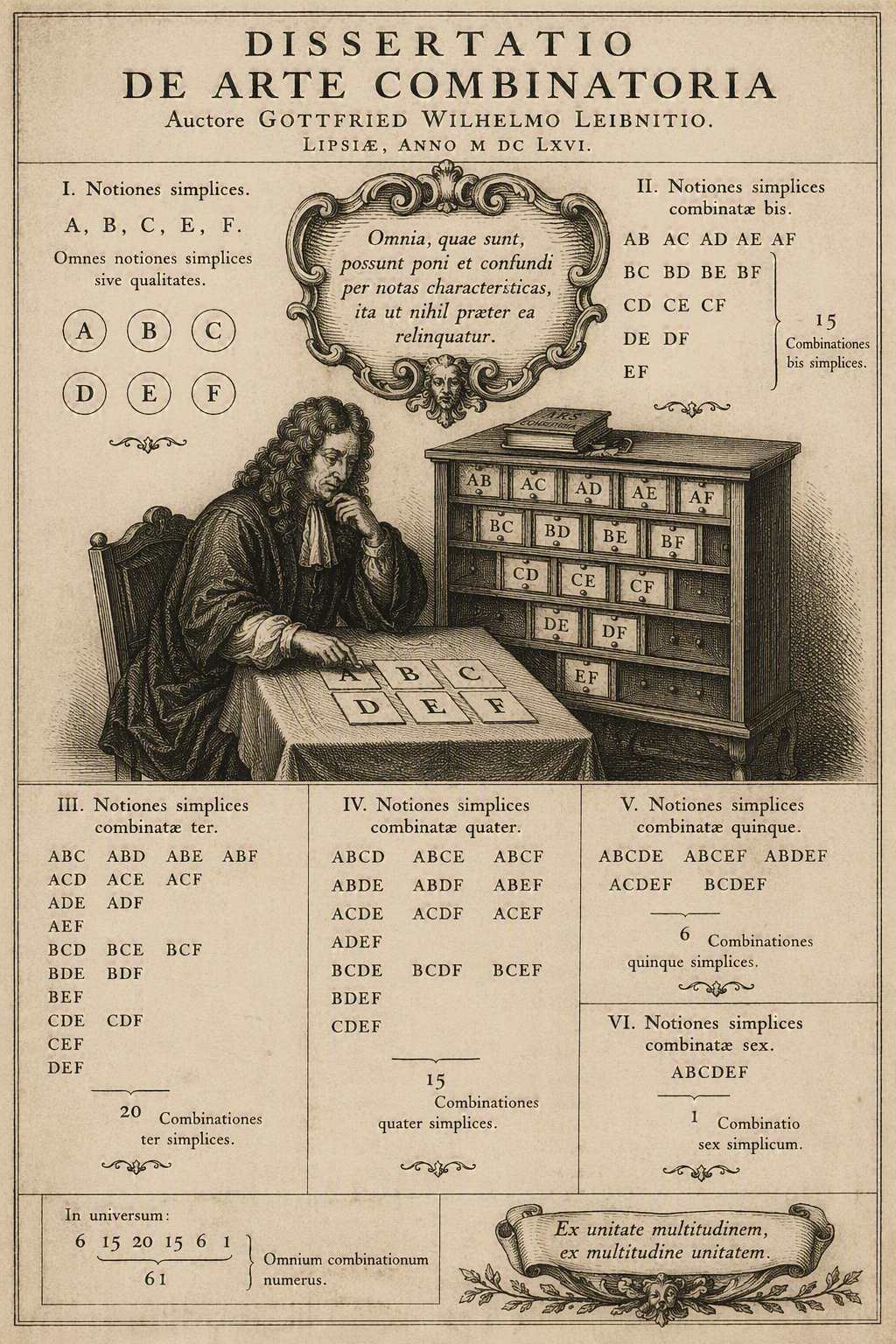

Leibniz never fully formalized this theory. His ideas on legal probability are scattered across letters, unpublished manuscripts, and doctoral dissertations written in his twenties. His legal writings — particularly the Dissertatio de Arte Combinatoria (1666) and various works on jurisprudence — apply combinatorial and probabilistic reasoning to legal evidence, but they never coalesce into a systematic treatise. Leibniz had a lifelong habit of beginning ambitious projects and leaving them unfinished as the next idea arrived. He died in 1716 in Hanover, largely forgotten by the court that had employed him for decades, his room reportedly unvisited at the end, while his employer George I had moved to England to take the British throne. His secretary and a single servant attended the funeral.

Leibniz never fully formalized this theory. His ideas on legal probability are scattered across letters, unpublished manuscripts, and doctoral dissertations written in his twenties. His legal writings — particularly the Dissertatio de Arte Combinatoria (1666) and various works on jurisprudence — apply combinatorial and probabilistic reasoning to legal evidence, but they never coalesce into a systematic treatise. Leibniz had a lifelong habit of beginning ambitious projects and leaving them unfinished as the next idea arrived. He died in 1716 in Hanover, largely forgotten by the court that had employed him for decades, his room reportedly unvisited at the end, while his employer George I had moved to England to take the British throne. His secretary and a single servant attended the funeral.

What Leibniz was describing — even if he never completed the mathematics — was what would later be called subjective probability: the idea that a probability is a rational agent's degree of belief in a proposition, held firmly enough to act on and loosely enough to revise when new evidence arrives. Thomas Bayes would give this idea its mathematical machinery a generation later. Pierre-Simon Laplace would extend it into a comprehensive framework. But Leibniz articulated the philosophical foundation: that uncertainty is not binary but continuous, that it can be measured, and that the measure should change as evidence accumulates.

He also, in a characteristic act of intellectual omnivore ambition, connected this to his broader metaphysics. His famous claim that we live in the best of all possible worlds — the claim Voltaire savaged so mercilessly in Candide — was not naive optimism. It was a probabilistic statement: given all the constraints a creator faces, this world is the one with the highest probability of being good. Probability, for Leibniz, was not just a tool for gamblers or lawyers. It was built into the structure of rational thought itself.

◆ The Legacy

The calculus dispute with Newton — conducted partly by proxy, partly through anonymous pamphlets that Leibniz himself wrote under false names, and concluded in 1711 when the Royal Society declared Newton the prior inventor — consumed the final years of Leibniz's life and damaged his reputation in England irreparably. Modern scholarship holds that both men developed calculus independently, and it is Leibniz's notation — the d and the integral sign — that every student in the world now uses. His binary number system underpins all modern computing. His logic anticipates the work of Boole and Frege by two centuries. His probability theory anticipates Bayes and Laplace. He is, by any reasonable accounting, one of the most consequential thinkers in the history of Western thought — and yet he remains less known than any of them, in part because his work was so scattered, so unpublished, so resistant to the kind of single landmark achievement that history remembers easily.

◆ Your Money

Leibniz's degrees of certainty translate directly into investment practice — and into the most important distinction a serious investor can make.

Most investment decisions are not like dice rolls. You cannot repeat the experiment ten thousand times to observe the frequency of outcomes. You are asking, instead: given what I know right now, how confident should I be that this manager has genuine skill rather than good luck? That this asset class will outperform over the next decade? That this economic scenario will materialize? These are questions about degrees of certainty — Leibniz's domain.

The reasonable response to that kind of uncertainty is not a confident prediction but a calibrated belief: held firmly enough to allocate capital, loosely enough to revise when the evidence changes. The investor who cannot distinguish between "I am 90 percent confident" and "I am 55 percent confident" — who treats every conviction as either certain or dismissible — is not reasoning about probability at all. They can be seen as collapsing Leibniz's spectrum into a binary, discarding almost all the information that rational analysis could provide.

Many evidence-based investors do the opposite. They hold beliefs as probabilities, update them as evidence accumulates, and build portfolios that are robust to being wrong at the margin rather than dependent on any single conviction being exactly right. That is the spectrum in practice. That is what Leibniz was describing, two and a half centuries before behavioral finance gave us the vocabulary to diagnose its absence.

Sources: Leibniz, G. W. (1989). Philosophical papers and letters (L. Loemker, Ed. & Trans.). Kluwer. Hacking, I. (1975). The emergence of probability. Cambridge University Press. Franklin, J. (2001). The science of conjecture. Johns Hopkins University Press.

Disclosure: This article is for informational and educational purposes only and does not constitute a solicitation or recommendation to buy or sell any security. Past performance is not indicative of future results. All investing involves risk, including the possible loss of principal. Any historical return examples, if referenced, are hypothetical illustrations based on published index data and are not reflective of actual investor experience

Content is AI-assisted. Index Fund Advisors, Inc. is a registered investment adviser. For additional information, please visit adviserinfo.sec.gov or www.ifa.com.

About the pen name: "Claude Hebner" represents a collaboration between Mark Hebner, founder and CEO of Index Fund Advisors, Inc., and Claude, Anthropic's AI. The research, historical narrative, and investment analysis in each article are the result of that partnership — human editorial judgment and decades of financial expertise combined with AI-assisted research and drafting.

X

X