The story of the coin does not begin with metal. It begins with the human need to trade, to measure value, and to trust. Long before the first stamped disc changed hands, Africa was already running one of the world's most sophisticated monetary systems — one that predates the Lydian electrum stater by thousands of years.

Part I: Before the Coin — Africa's World of Commodity Money

Across sub-Saharan Africa, commodity currencies performed every function we now assign to coins. The cowrie shell (Cypraea moneta) — small, uniform, and nearly impossible to counterfeit — traveled inland from the Indian Ocean and the Maldives through vast trade networks. Their value was stable enough that kingdoms used them to pay soldiers, collect taxes, and ransom captives. Ancient China, India, and Africa all placed cowries at the center of their early monetary systems, but in Africa the cowrie persisted longer and traveled farther than almost anywhere else on earth.

In the gold-rich kingdoms of West Africa, gold dust weighed on precision scales was managed with the Akan people's gold weights (abrammuo): small brass figurines encoding exact measures of value, works of art and instruments of commerce simultaneously — a combination the coin would later inherit. Salt, harvested from the great Saharan deposits, functioned as a kind of solid currency, literally worth its weight in trade across the continent. Copper crosses known as the Katanga Cross circulated across Central and Southern Africa stretching from the Congo Basin into Zimbabwe and Mozambique. Iron, cloth, cattle, and manilla bracelets all served monetary roles in different regions, with local rulers managing exchange rates between currency zones. Africa was not waiting to be introduced to commerce — it was already operating a diversified, sophisticated monetary landscape when the first stamped coins appeared elsewhere in the ancient world.

Part II: The First Coins — Lydia and the Ancient World (~630–500 BC)

The Lydian electrum stater, c. 630–620 BC — the world's first officially minted coin. Stamped with a roaring lion's head, the royal symbol of King Alyattes, it certified weight and purity with the authority of the crown. Minted in Sardis, Lydia (present-day western Turkey).

The honor of minting the world's first official coin belongs to the kingdom of Lydia in what is now western Turkey, around 630–620 BC. King Alyattes ordered the production of small, bean-shaped lumps of electrum — a natural gold-silver alloy — stamped with a roaring lion's head, the royal symbol of the Lydian dynasty.

This was a revolutionary act. Before Lydia, metal was weighed out for each transaction — imprecise and trust-demanding. The king's stamp certified weight and purity, transforming a commodity into currency backed by royal authority. His son Croesus refined the system into the world's first bimetallic coinage of pure gold and silver — giving rise to the expression "rich as Croesus" still in use today. The Lydian stater set the template for virtually all coinage that followed.

The idea spread rapidly across the ancient world. Greek city-states adopted the model — Ephesos with its bee, Miletos with its lion, Phokaia with its seal — and by the 5th century BC the Athenian tetradrachm, bearing the helmeted head of Athena and her sacred owl, had become the trusted dollar of the Mediterranean world, accepted from Egypt to the Black Sea. Alexander the Great globalized coinage after conquering Persia in 330 BC, melting the imperial treasury into coins bearing his own portrait — the first living ruler to do so — a practice that defined royal coinage for two millennia. Rome's silver denarius (from 211 BC) became the economic backbone of Western civilization for four centuries; the emperor's face on every coin served as mass media across a largely illiterate empire, broadcasting legitimacy, divinity, and authority to millions of subjects who would never see their ruler in person.

Africa produced its own great minting tradition. The Kingdom of Aksum in present-day Ethiopia began striking gold, silver, and bronze coins around AD 270 — Africa's first indigenous mint. Aksumite coins bore royal portraits and, after the kingdom's conversion in the 4th century, Christian crosses — remarkably early propaganda for the new faith. These coins circulated in the Red Sea trade routes, accepted from Egypt to India, and remain an invaluable record of an African empire that chose coinage as a deliberate instrument of international commerce.

Part III: The Medieval World — Islam, Gold, and Europe (AD 600–1500)

After the collapse of the Western Roman Empire in the 5th century, coinage did not disappear — it transformed. The Byzantine solidus anchored Mediterranean trade for 700 years, so consistently pure that merchants from Western Europe to Arabia hoarded it as a monetary reserve. The rise of Islam after the 7th century produced a rival monetary order: in AD 697, the Umayyad Caliphate issued the first purely Islamic coins — the dinar (gold) and dirham (silver) — stripped of all figural imagery and inscribed instead with Arabic calligraphy and Quranic verses. It was a radical declaration that this civilization would not picture its rulers on money. Islamic dinars circulated from Spain to Southeast Asia and deep into West Africa, exchanged for gold dust along the trans-Saharan routes.

The Mali Empire under Mansa Musa — whose legendary 1324 pilgrimage to Mecca, accompanied by tens of thousands of attendants and hundreds of camels laden with gold, reportedly depressed gold prices across North Africa and the Middle East for years — participated in this global coin economy while maintaining indigenous cowrie and gold-dust currencies internally. His journey illustrated the degree to which African economies were already integrated into the world monetary system.

In Europe, the reintroduction of gold coinage in the 13th century signaled the continent's economic recovery from the post-Roman collapse. The Florentine florin (1252) and Venetian ducat (1284) — pure gold, consistent weight, minted to an unwavering standard — became the euros of medieval commerce, trusted by merchants from London to Constantinople. Bankers began tracking exchange rates, discounting debased coins, and speculating on bullion flows. By the 14th century the modern concept of the coin as a financial instrument subject to inflation, debasement, and market forces was fully established.

Part IV: The Age of Exploration — Spain, Silver, and the Piece of Eight (1400–1800)

When Spanish conquistadors opened the Americas in the early 16th century, they unlocked the largest concentration of silver the world had ever known. In 1545, the discovery of Cerro Rico — the "Rich Hill" — in what is now Bolivia led to the founding of Potosí, a city that exploded to 160,000 inhabitants, one of the largest on earth. Between 1556 and 1783, Cerro Rico yielded an estimated 41,000 metric tons of silver. The Casa de la Moneda de Potosí, established in 1572, ran on the forced labor of enslaved African men and Indigenous workers conscripted through the brutal mita system. As many as eight million people may have died working these mines.

The coins produced — macuquinas or cobs — were made by hammering rough silver chunks between two dies and trimming them to weight. The largest, the 8 reales or piece of eight, became history's first truly global currency, accepted from China to colonial America. The dollar sign "$" is widely believed to derive from the Pillars of Hercules on its face. When the United States defined its dollar in 1792, it set the value at par with the Spanish piece of eight.

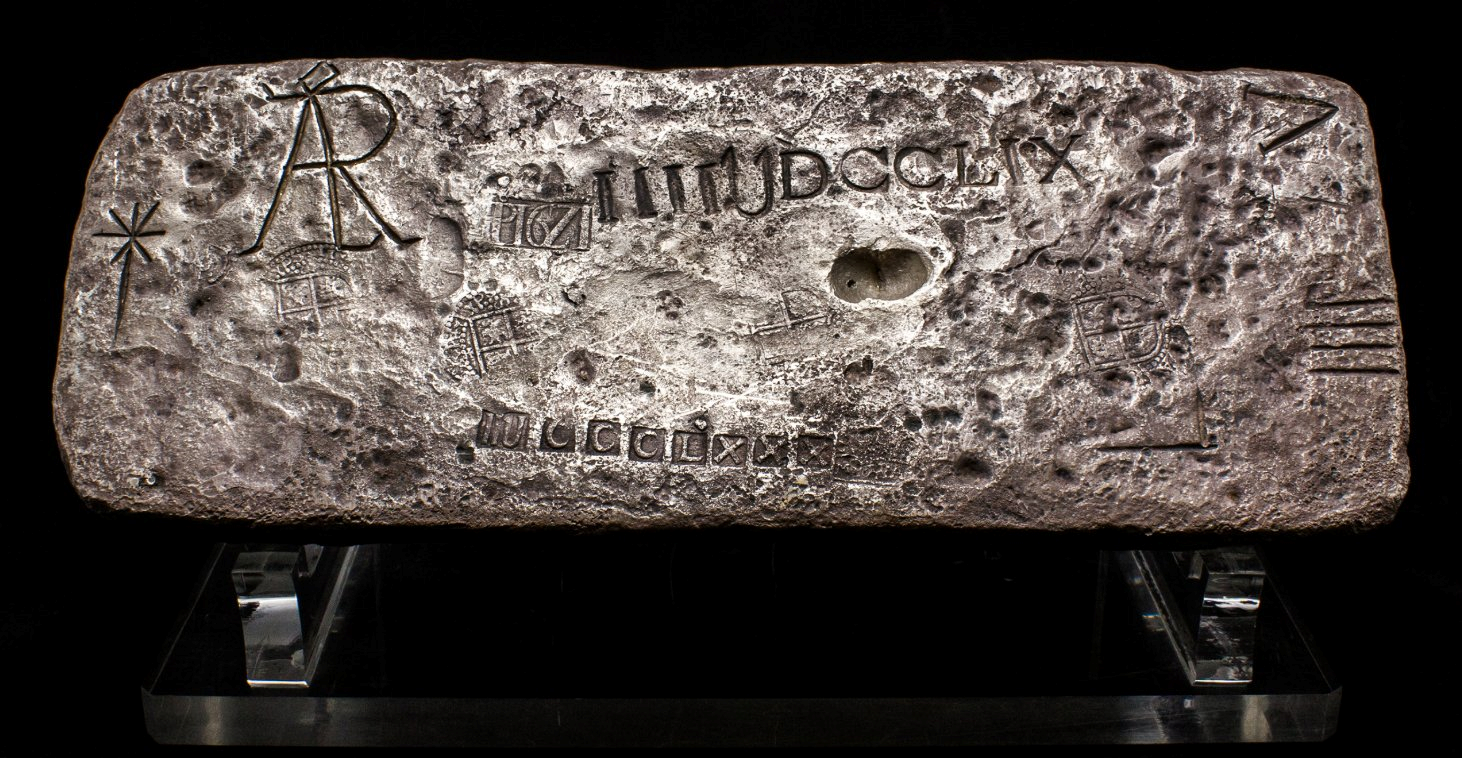

A piece of eight (8 reales cob) recovered from the Nuestra Señora de Atocha. The royal arms of Spain are visible on one side.

The reverse of an Atocha cob, showing the characteristic quartered cross — each coin unique, trimmed by hand to the correct weight.

The Nuestra Señora de Atocha

The most famous vessel of the Fleet of the Indies was the Nuestra Señora de Atocha, a 500-ton warship built in Havana in 1620. In summer 1622 she took on a staggering cargo: 964 silver bars, 255,000 silver coins, 161 gold bars and discs, 1,200 pounds of worked silverware, and smuggled emeralds — estimated at $250–$500 million in modern value. Departing Havana on September 4, 1622, already weeks late into hurricane season, the fleet was struck by a full-force storm on September 6. The Atocha sank in 55 feet of water near the Marquesas Keys, Florida. Of 265 people aboard, only five survived.

A silver bar from the Atocha, stamped with assay marks, tax stamps, and the shipper's registration number — each mark a record of its journey from Potosí mine to Spanish galleon.

Another Atocha silver bar bearing the distinctive stamping of the Potosí mint. These bars were cast from Andean ore, certified by colonial assayers, and destined for the Spanish treasury.

|

A silver pitcher from the Atocha. Among the 1,200 pounds of worked silverware aboard, pieces like this belonged to wealthy passengers — the personal treasure of a colonial elite. |

A silver plate from the Atocha, corroded by three and a half centuries on the ocean floor. |

|

The Swept Hilt Rapier — a 16th-century Toledo Steel fencing sword recovered in 1985 from the Nuestra Señora de Atocha, sunk 1622. |

|

Spain searched for 60 years and never found the wreck. In 1969, treasure hunter Mel Fisher began a sixteen-year obsession from Key West. His daily mantra — "Today's the day!" — drove the search through devastating personal loss, including the drowning of his son Dirk in 1975. On July 20, 1985, Fisher's son Kane radioed: "Put away the charts — we've found the main pile!" Fisher ultimately recovered 47 tons of silver and gold, 70 pounds of emeralds, and over 100,000 artifacts, estimated at $450 million — at the time the most valuable shipwreck ever found.

The global impact of Spanish silver was staggering. Spain extracted more silver between 1500 and 1800 than the entire rest of the world had produced in all of prior history. In Europe, the flood of New World metal caused a century-long Price Revolution — sustained inflation that eroded feudal wealth and helped undermine the old social order. An estimated one-third of all Potosí's output crossed the Pacific on the Manila Galleon route, traded for Chinese silk, porcelain, and spices in an annual exchange that connected the mines of Bolivia to the workshops of Guangdong. The piece of eight was so dominant that it remained legal tender in the United States until 1857. This era also deepened Africa's tragic role in the global coin economy: European silver became the medium through which an estimated 12 million enslaved people were purchased and transported across the Atlantic between the 15th and 19th centuries. The coin, in this chapter of history, bore the weight of enormous suffering.

Part V: Central Banks, Gold Standard, and the Digital Age (1800–Present)

The 19th century brought central banking, the gold standard, and the gradual relegation of coins from primary monetary instruments to fractional change. As paper banknotes — backed first by gold reserves and later by government authority alone — took over large-value transactions, coins shrank in denomination and grew in symbolic importance. Colonial powers across Africa imposed their own coin systems not merely for commerce but as instruments of political control. The requirement to pay taxes in colonial currency forced African farmers into wage labor and cash-crop production, systematically dismantling millennia of diverse indigenous monetary systems — cowrie economies, gold-dust exchange, and copper-cross networks that had functioned effectively for generations.

After World War I, the gold standard began its slow collapse under the weight of wartime debt and deflationary pressure. The Great Depression shattered confidence in fixed exchange rates. In 1971, President Nixon formally ended the dollar's convertibility to gold, completing a transformation that had been building for centuries: money was now pure convention, backed by nothing more — or less — than the collective agreement of billions of people. Modern coins are copper-nickel tokens whose value rests entirely on public trust, the same fundamental ingredient that gave authority to every cowrie shell and electrum stater before them.

The 21st century brought cryptocurrency — Bitcoin and its successors reviving ancient questions about scarcity, counterfeiting, and what legitimizes money in the first place. Yet alongside that digital revolution, a very different kind of coin was being created, rooted not in speculation but in rigorous mathematical proof and investor education.

Part VI: The IFA MarketCoin — Where Probability Meets the Market

In the long history of the coin — from Lydian electrum to Roman denarius, from Islamic dinar to Spanish piece of eight, from colonial franc to digital token — every coin has been an instrument for managing uncertainty. Every transaction is a bet: a buyer and a seller, each believing the exchange serves their interest. What changes across history is our understanding of how uncertainty actually works, and whether we can measure it honestly.

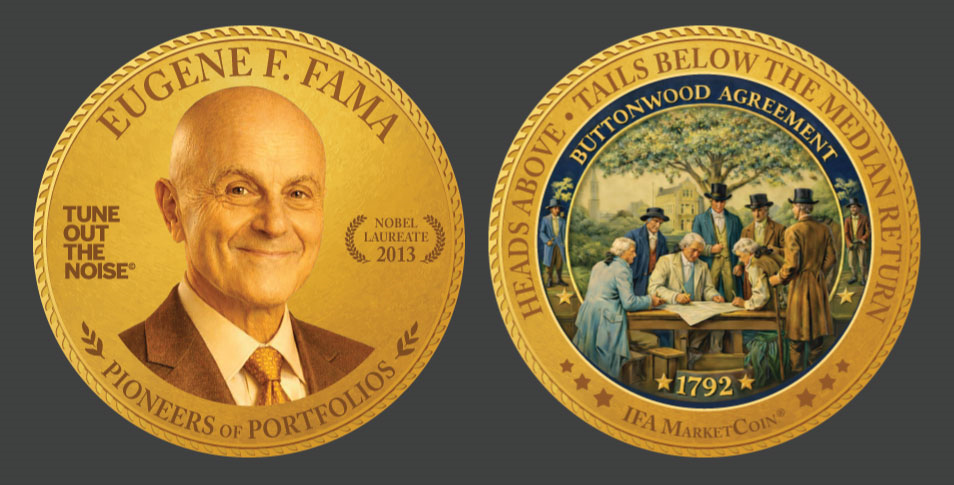

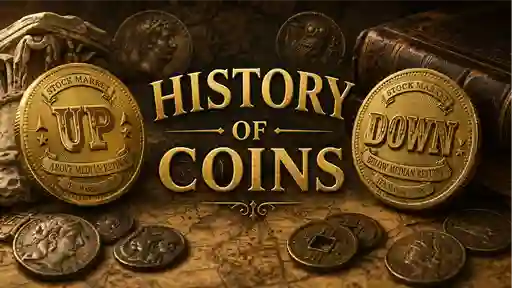

Mark T. Hebner, founder and CEO of Index Fund Advisors, Inc. (IFA), created the IFA MarketCoin as a direct expression of that understanding. Where the Lydian stater was stamped with a lion to certify metal content, and the Spanish piece of eight bore the Pillars of Hercules to announce imperial authority, the MarketCoin is inscribed with the language of probability. One side reads "Above the Median Return"; the other reads "Below the Median Return" of a market index such as the S&P 500.

The IFA MarketCoin® — two sides of the same probability. One flip, one outcome: Stock Market Up (Above Median Return) or Stock Market Down (Below Median Return). Each is equally likely relative to the historical median return.

The coin's design is rooted in the Efficient Market Hypothesis (EMH), the framework developed by Nobel laureate Eugene Fama at the University of Chicago, which holds that in a well-functioning market, prices are generally understood to reflect available information at any given moment. Millions of willing buyers and sellers, each acting in their own interest, rapidly incorporate every piece of publicly available information into prices. The consequence is that future price movements are driven only by new information — which, by definition, cannot be known in advance. The direction of the next return is therefore not predictably knowable in advance, much like the flip of a fair coin.

A critical nuance distinguishes the MarketCoin from a simple coin flip: the market is not expected to return zero. Economists recognize equity markets as a "sub-martingale" — a stochastic process whose expected future value exceeds its current value because investors require compensation for bearing risk. The relevant benchmark is therefore not zero but the median return: the positive, risk-appropriate return that investors can reasonably expect from a diversified portfolio over time. The MarketCoin's two sides — "Above the Median Return" and "Below the Median Return" — are calibrated to this positive expected return. The coin does not ask whether the market will rise or fall in absolute terms; it asks whether returns will land above or below the median of their historical distribution, centered on a positive expected reward for taking risk. That distinction is everything.

The median does more than split sorted historical returns exactly in half. Markov Chain analysis of actual market data is consistent with a 50/50 split holds at every step in the sequence. Whether a given period's return landed above or below the median, the probability that the next period's return will be above the median is 50%, and the probability it will be below is 50%. Up follows Up 50% of the time. Up follows Down 50% of the time. Down follows Up 50% of the time. Down follows Down 50% of the time. Each state — Up or Down relative to the median — is followed by a 50/50 chance of the next state. The market exhibits no exploitable memory within this probabalistic framework. This is the mathematical heart of the random walk, and the reason the MarketCoin is not merely a metaphor but a precise statistical model of how markets actually behave.

Eugene F. Fama — Nobel Laureate 2013. The reverse features the Buttonwood Agreement of 1792 — the founding moment of what became the New York Stock Exchange — framed by the coin's core message: "Heads Above · Tails Below the Median Return." Pioneers of Portfolios Series.

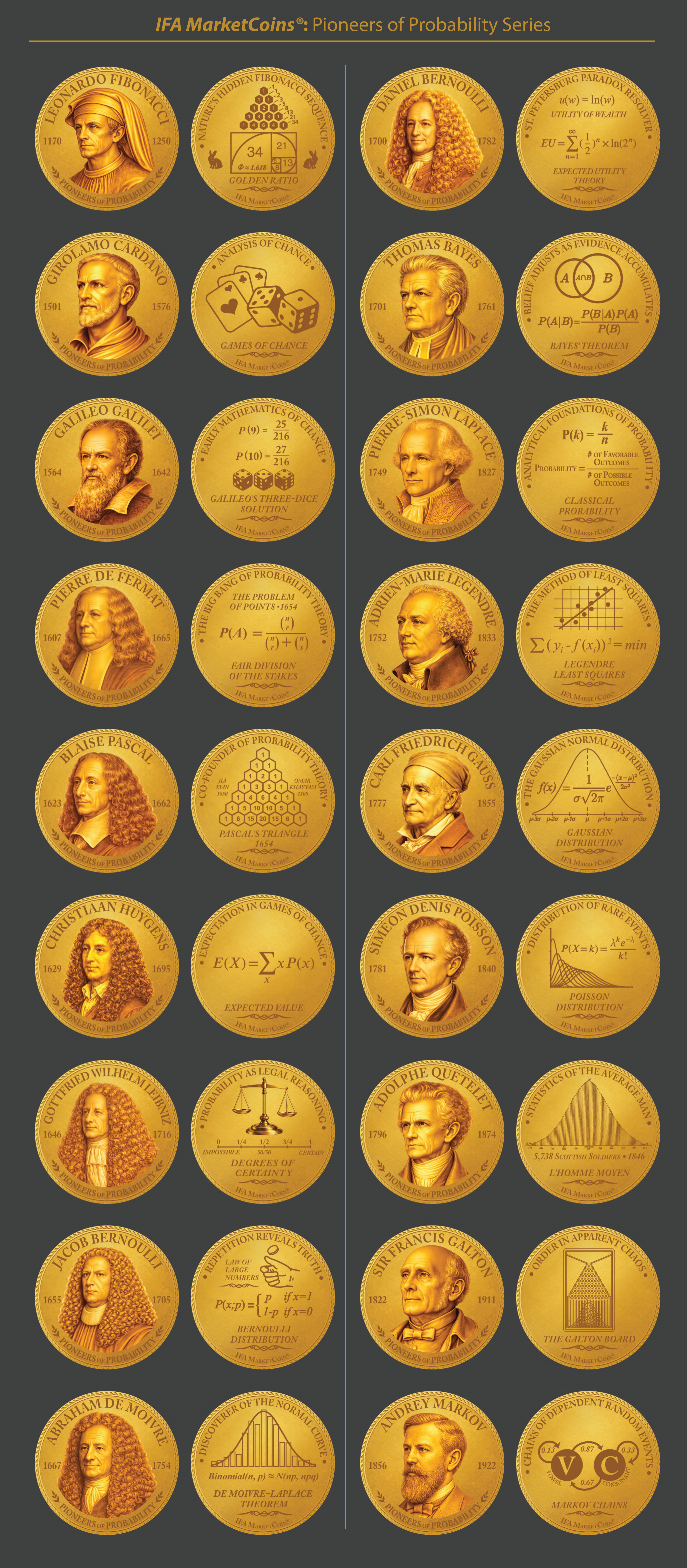

The Pioneers of Probability Series

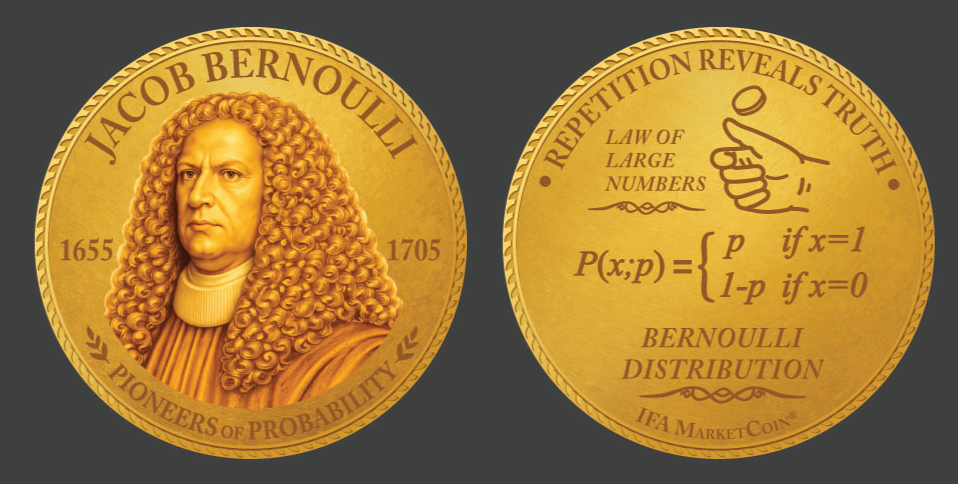

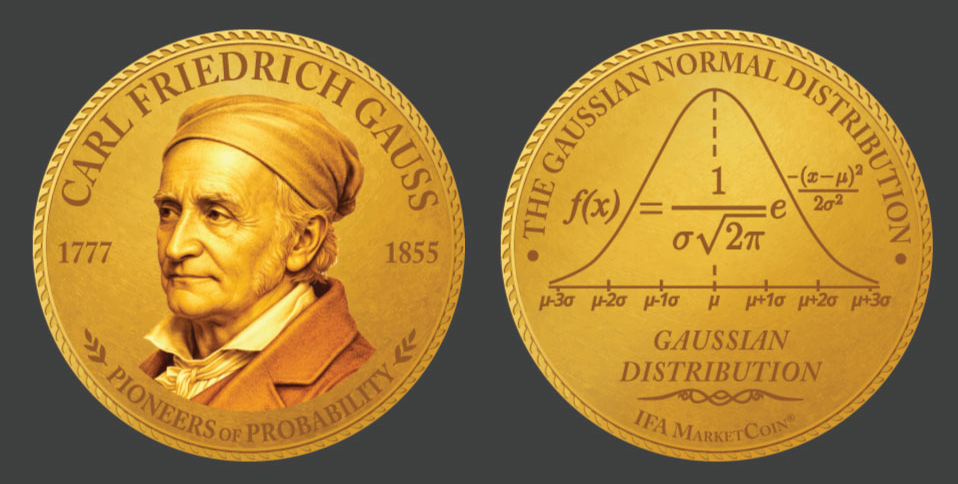

IFA has developed the MarketCoin into a Pioneers of Probability Series, honoring the mathematicians whose work built the probabilistic framework underlying modern investing. Blaise Pascal and Jacob Bernoulli established early probability theory through the study of games of chance. Abraham de Moivre described the normal distribution — the bell curve that governs the spread of market returns. Carl Friedrich Gauss formalized its mathematics. Sir Francis Galton invented the Galton Board, which physically demonstrates how random binary events accumulate into a bell curve. Eugene Fama formalized the Efficient Market Hypothesis, proving that prices already incorporate all available information. Each coin in the series links one of these eighteen thinkers — from Fibonacci through Markov — to a specific foundational concept, tracing the intellectual lineage of evidence-based investing.

Blaise Pascal (1623–1662) — Co-Founder of Probability Theory. The reverse features Pascal's Triangle (1654). IFA MarketCoin® Pioneers of Probability Series.

Jacob Bernoulli (1655–1705) — "Repetition Reveals Truth." The reverse displays the Bernoulli Distribution and the Law of Large Numbers. IFA MarketCoin® Pioneers of Probability Series.

Carl Friedrich Gauss (1777–1855) — The Gaussian Normal Distribution, the mathematical foundation for understanding the distribution of market returns. IFA MarketCoin® Pioneers of Probability Series.

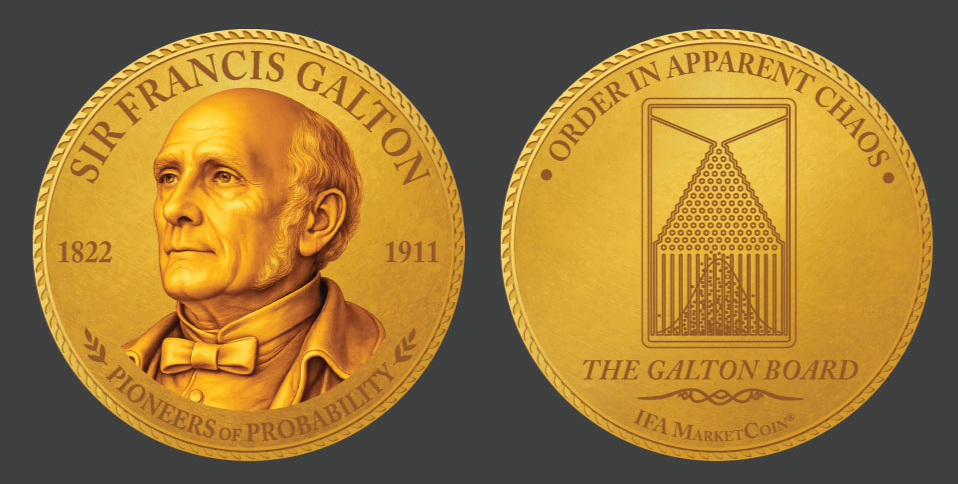

Sir Francis Galton (1822–1911) — "Order in Apparent Chaos." The reverse depicts the Galton Board, whose falling beads produce a bell curve matching the distribution of long-run market returns. IFA MarketCoin® Pioneers of Probability Series.

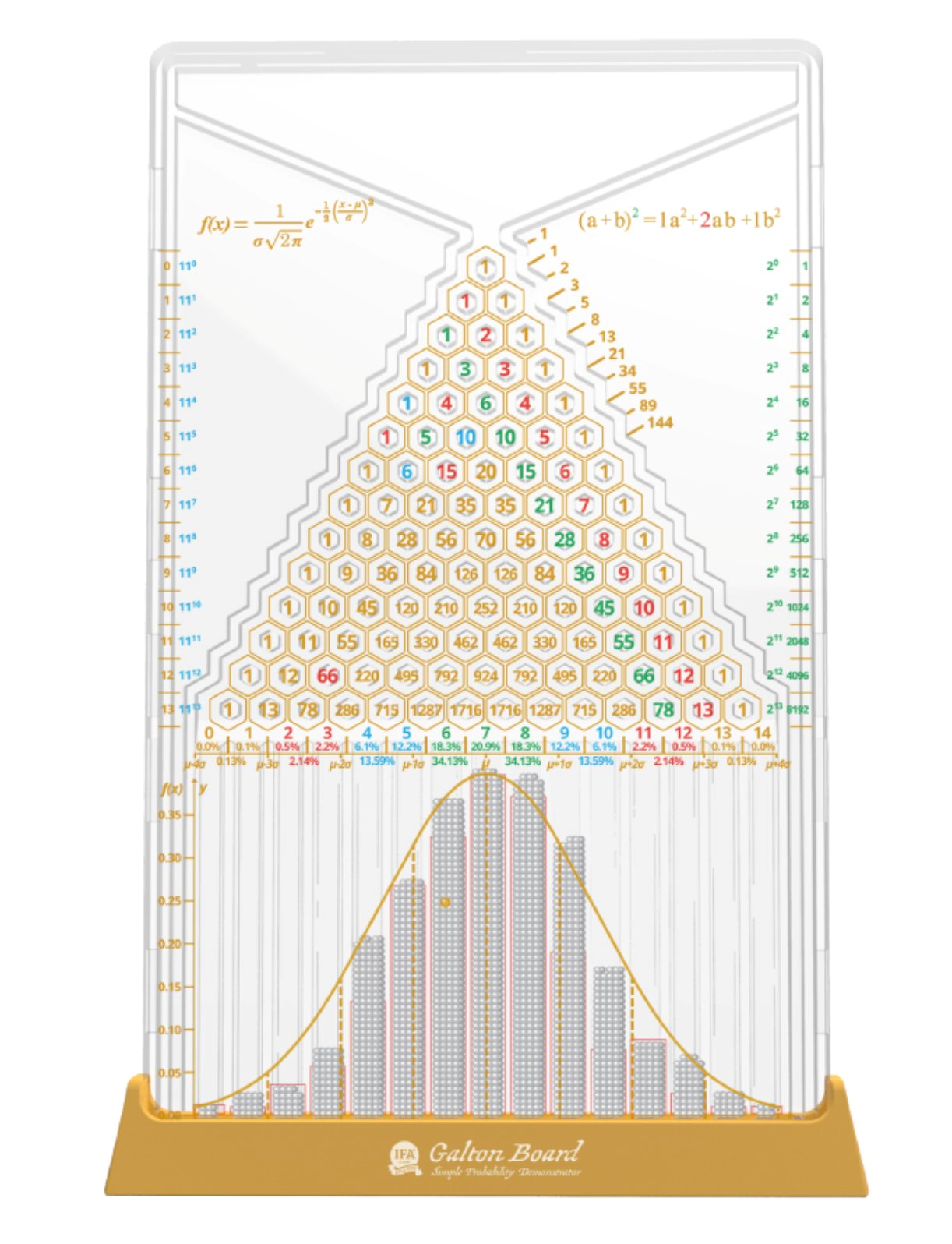

The MarketCoin pairs with IFA's Galton Board — the physical device whose falling beads produce a bell curve — to form a complete educational system. The Galton Board shows the shape of the distribution of market returns over time; the MarketCoin demonstrates that any single outcome within that distribution is unpredictable. Together they embody what every great monetary innovator in this history was ultimately working toward: a trustworthy, honest representation of value and its limits.

The IFA Galton Board — Simple Probability Demonstrator. Falling beads make a binary left/right decision at each hexagonal peg — exactly like a coin flip — and accumulate into a bell curve below, physically demonstrating how countless independent random events produce the normal distribution that governs long-run market returns.

Markov Chain analysis of 6,583 trading days (IFA Portfolio 100, 3/1/2000–5/4/2026) illustratesthe 50/50 rule: each transition — Up to Up, Up to Down, Down to Up, Down to Down — occurs approximately 50% of the time relative to the median return. The market has no memory.

The Pioneers of Portfolios Series (aka Tune Out the Noise Series)

The second major series shifts from the history of mathematics to the history of modern portfolio theory. The Pioneers of Portfolios Series — also known as the Tune Out the Noise Series — honors the economists, academics, and practitioners who translated probabilistic thinking into the practical science of index investing. The series includes Nobel laureates Eugene Fama, Robert Merton, Paul Samuelson, and Myron Scholes; pioneering researchers Kenneth French, Roger Ibbotson, and Robert Novy-Marx; and the practitioners and leaders — David Booth, Rex Sinquefield, Dan Wheeler, Jeanne Sinquefield, Savina Rizova, Mark Hebner, and others — who built the institutions and strategies that put these ideas to work for investors. The reverse of every coin in this series depicts the Buttonwood Agreement of 1792, the founding moment of what would become the New York Stock Exchange, flanked by the coin's core message: "Heads Above • Tails Below the Median Return."

IFA MarketCoins® — Pioneers of Portfolios Series (Tune Out the Noise Series). Nobel laureates, researchers, and practitioners who built the science and institutions of index investing, from Paul Samuelson and Eugene Fama to David Booth, Mark Hebner, and beyond.

The 12-Step Series

The 12-Step Series translates IFA's twelve-step investment program into coin form. Each pair of coins illustrates one step in the evidence-based investor's journey — from recognizing the failure of active management and stock picking, through understanding risk and diversification, to the discipline of rebalancing and tax-loss harvesting. The coins feature original paintings commissioned to dramatize each step: a gambler at the roulette table for stock picking, a siren song for market timing, and a golden egg for the long-term compounding reward that awaits those who stay the course. Every coin carries the same message on its reverse: Above or Below the Median Return.

IFA MarketCoins® — 12-Step Series. Each pair of coins illustrates one of IFA's twelve steps from active investing to evidence-based index investing, featuring original commissioned paintings that dramatize the behavioral and structural traps every investor must navigate.

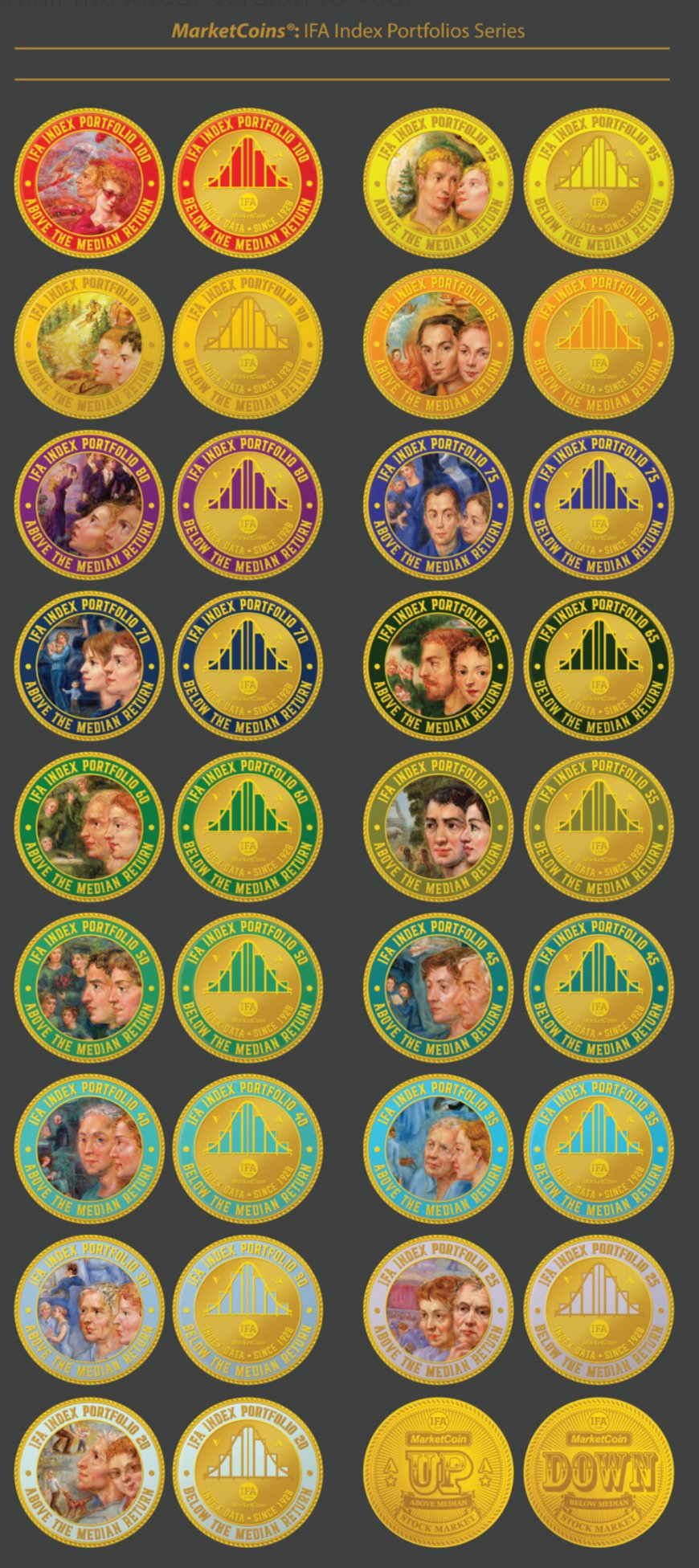

The IFA Index Portfolios Series

The IFA Index Portfolios Series completes the collection by mapping the full spectrum of IFA's twenty risk-based index portfolios onto individual coins. Each portfolio — from the most conservative (IFA Index Portfolio 5) to the most aggressive (IFA Index Portfolio 100) — has its own coin, with the obverse featuring a distinctive color-coded portrait and the reverse displaying IFA's bar chart of historical return distributions. Every coin in the series carries the same probabilistic message: Above or Below the Median Return. Together the series gives investors a tangible, physical representation of where their own portfolio sits on the risk-return spectrum — and a daily reminder that wherever they sit, the next period's result is a 50/50 proposition relative to that portfolio's median.

IFA MarketCoins® — IFA Index Portfolios Series. Twenty coins spanning IFA Index Portfolios 5 through 100, each color-coded to its risk level. Every coin carries the same 50/50 median-return message, grounding each investor's risk choice in the same probabilistic reality.

Conclusion: A Coin Always Carries a Question

From the cowrie shells of West Africa to the Lydian lion, from the Aksumite gold stater to the Spanish piece of eight, from the colonial franc to the IFA MarketCoin, every coin in history has encoded the same question: what is this worth, and can I trust it?

The answers have shifted with each civilization — trust stamped by a king, broadcast by an emperor's portrait, certified by an assayer's initials, anchored to gold, and finally resting on nothing more than collective agreement. What is remarkable across this 75,000-year journey — from the first shell beads to the latest digital token — is how consistent the underlying logic has been. Every successful monetary instrument has needed to be portable enough to carry, durable enough to last, scarce enough to hold value, and recognizable enough to be accepted by a stranger. A cowrie shell from West Africa and a piece of eight from Potosí are separated by thousands of years and entirely different civilizations, yet they answer the same question in the same structural way.

The IFA MarketCoin adds one final layer. It is the first coin in this history that honestly represents not just value, but the limits of our knowledge about value's future direction. Inscribed not with a monarch's portrait or a national emblem but with the probabilistic acknowledgment that the market's next move is above or below the median, it may be the most philosophically truthful coin ever struck. It makes no promises about outcomes. It teaches investors to reason carefully about probability — which is, in the end, what every careful student of money, from the first bead-makers of southern Africa to the index fund investors of today, has always had to learn to do.

Sources

Wikipedia (History of Coins, Lydia, Aksumite Currency, Nuestra Señora de Atocha, Spanish Dollar); World History Encyclopedia; Britannica; GIA; MelFisher.org; American Numismatic Association; Aeon Essays (Potosí); ifa.com/coins; ifa.com/articles/ifa-marketcoin-direction-of-market-returns

Disclosure:

This article is for educational purposes only and is not intended as investment advice or a recommendation to buy or sell any security. References to historical market behavior, probability, and statistical models are illustrative and do not guarantee future results. All investing involves risk, including the potential loss of principal. Market outcomes are uncertain, and past performance is not indicative of future performance.

X

X