Each year, the College for Financial Planning compiles a comprehensive list of contribution limits to everything from 401(k) plans and Individual Retirement Accounts to Medicare as well as health savings accounts.

As we did last year, IFA has worked with the college to turn such tables for 2026 contribution limits into a series of graphics.

Below is a breakdown with some key contribution limits in 2026. It's designed to act as a sort of 'cheat sheet' for you to discuss different financial and investment-related matters with IFA's team of wealth advisors and tax planners.

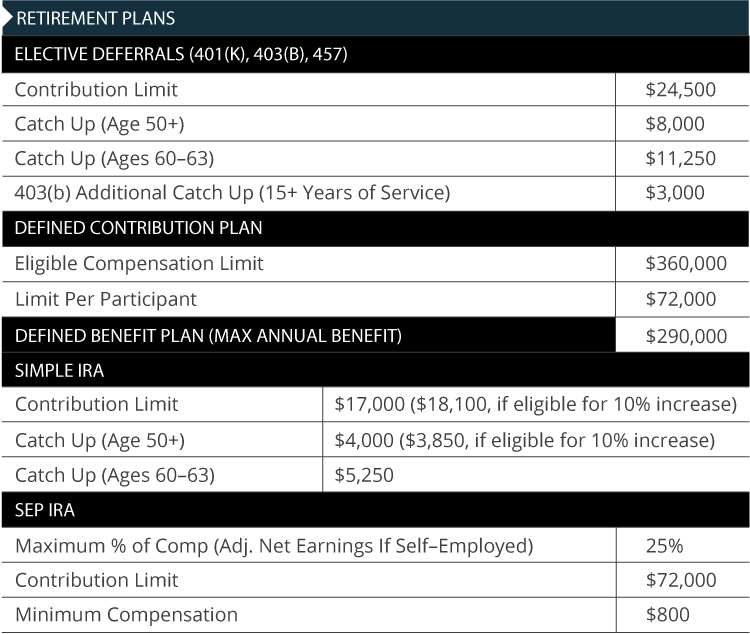

Retirement Plans

In 2026, elective deferrals to workplace retirement savings programs such as 401(k) and 403(b) plans are going up by $1000 to $24,500 a person for those under the age of 50. For those aged 50 and up, a worker can still contribute an additional $8,000, which is the same as in the previous year. That means total contributions for those aged 50 and older rise to $32,500 in 2026.

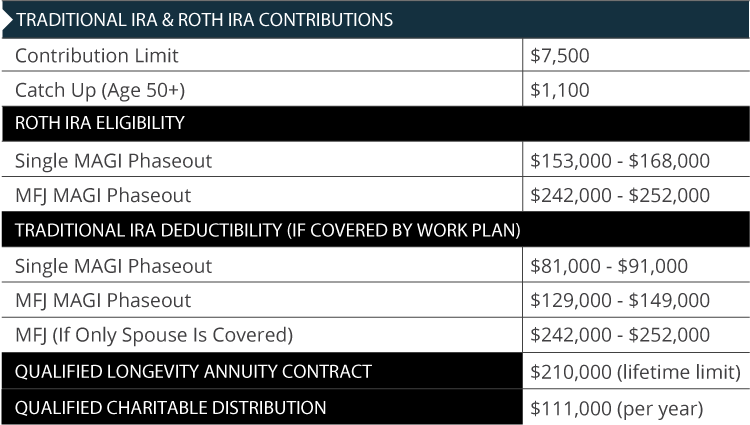

Also of note: IRA and Roth IRA contribution limits rose by $500 for 2026 at $7,500 per person. For those age 50 and older, the catch-up contribution increased by $100 to $1,100. Meanwhile, SIMPLE plan contributions rose by $500 per person in 2026 to $17,000 with the catch-up (50 or older) increasing to $4,000 per person.

*The catch-up contribution limit that generally applies for employees aged 50 and over who participate in most 401(k), 403(b), governmental 457 plans, and the federal government's Thrift Savings Plan increases to $8,000 for 2026. Therefore, participants in most 401(k), 403(b), governmental 457 plans and the federal government's Thrift Savings Plan who are 50 and older generally can contribute up to $32,500 each year, starting in 2026. Under a change made in SECURE 2.0, a higher catch-up contribution limit applies for employees aged 60, 61, 62 and 63 who participate in these plans. For 2026, this higher catch-up contribution limit stays at $11,250. Along with the increased contribution limits for 2026 of $24,500 plus super catch-up limit the total contribution limit allowed for for ages 60, 61, 62 and 63 totals $35,750.

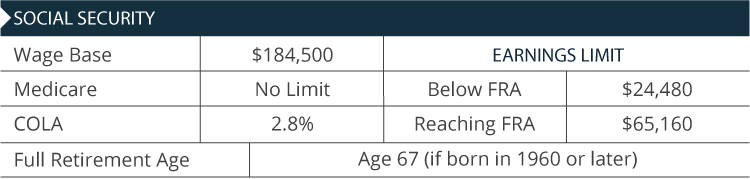

Social Security

In 2026, the taxable wage base went up by $8,400 to $184,500 a person. Another notable change was an increase of $134 a person to $4,152 in the maximum monthly benefit for a worker retiring at full retirement age. Meanwhile, Social Security's annual cost-of-living adjustment increased in 2026 to 2.8%, up from the previous year's 2.5% adjustment. (Note: FICA refers to the Federal Insurance Contributions Act and SECA is the Self Employed Contributions Act. Also, FRA stands for "Full Retirement Age.")

Estate & Gift Tax

The annual gift tax exclusion stayed the same at $19,000 and the maximum estate tax rate stayed at 40% in 2026. But the estate and gift tax exclusion rose to $15 million from the previous year's $13.99 million.

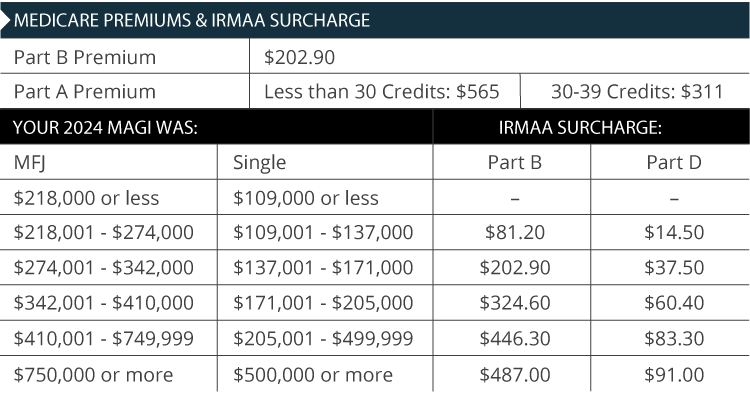

Medicare

The Part A standard monthly premium in 2026 increased slightly to a maximum of $565 (from $518 in 2025). At the same time, the base Part B monthly premium rose to $202.90 (from $185).

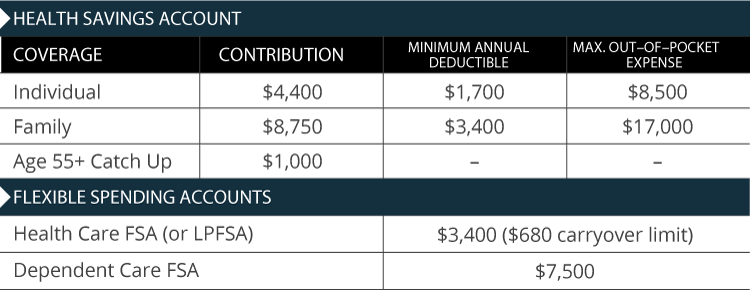

Health Savings Account

The minimum deductible amount for a single saver went up by $50 to $1,700 a person. For a family, it rose by $100 to $3,400. The maximum out-of-pocket amount has gone up — $200 more this year to $8,500 for a single person and $400 more to $17,000 for a family. The HSA statutory contribution maximum is also higher for a single saver ($4,400 vs. $4,300 in the previous year) and a family ($8,750 vs. $8,550). The catch-up contribution, however, for those age 55 or older stays at $1,000 in 2026.

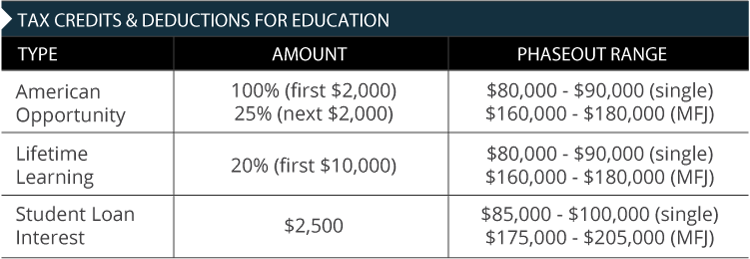

Education

The exclusion phaseout for the American Opportunity used for education by single tax filers stayed the same at $80,000-$90,000 in 2026. For those married filing jointly, the exclusion phaseout stayed at $160,000-$180,000. As shown in the table below, the phaseout ranges for the Lifetime Learning Credit also stayed the same in 2026 at $80,000-$90,000 for individuals and $160,000-180,000 for those married and filing jointly.

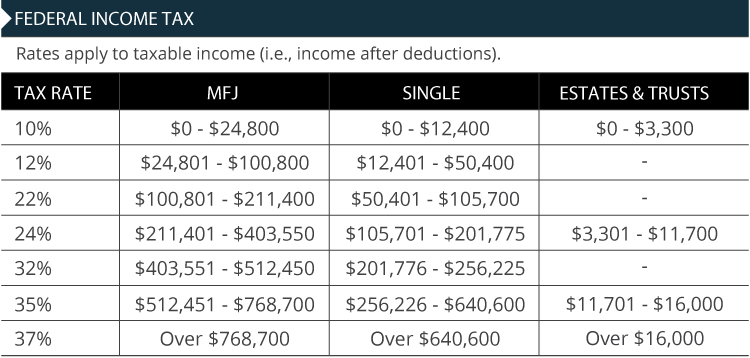

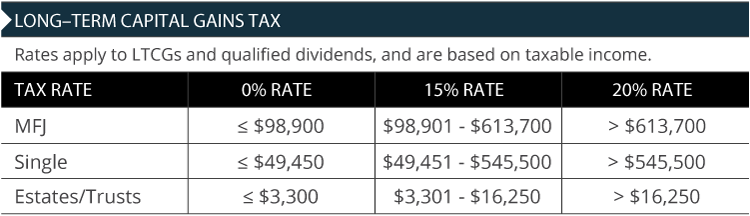

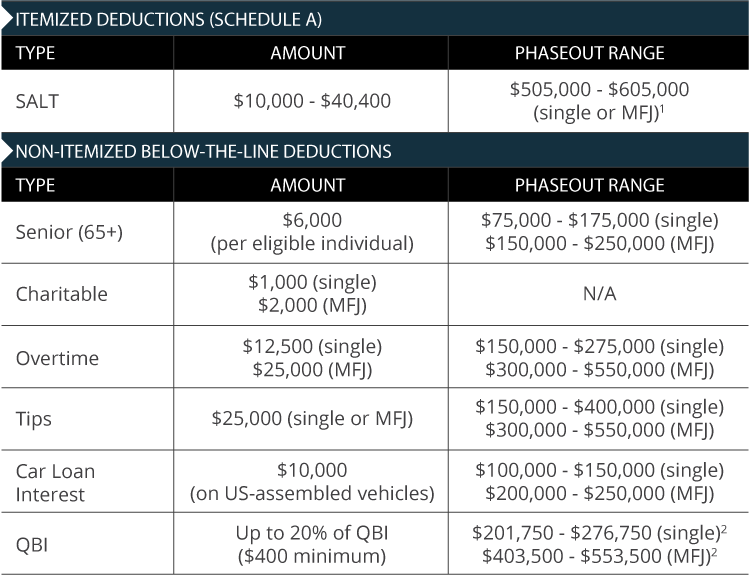

Income Taxes & Schedules

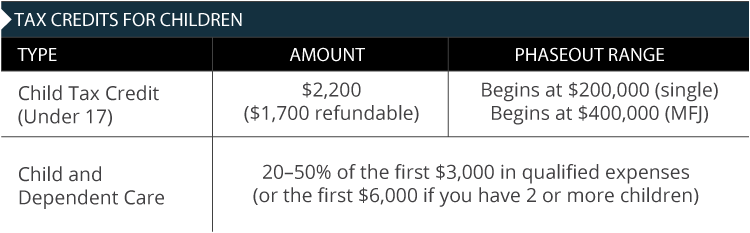

Tax Credits for Children

Other Items of Interest

This is intended to be informational in nature and should not be construed as an offer, solicitation, recommendation, endorsement of any security, or tax advice. As a division of Index Fund Advisors, Inc., IFA Taxes provides a wide array of tax planning, accounting and tax return preparation services for individuals and businesses across the United States. IFA Taxes does not provide auditing or attestation services and therefore is not a licensed CPA firm. IRS Circular 230 Disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. Federal tax advice contained in this communication is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter herein.

For more information about Index Fund Advisors, Inc, please review our brochure at https://www.adviserinfo.sec.gov/ or visit www.ifa.com.

X

X