The financial media loves heroes, but markets don't. A few managers will always look brilliant for a while; the real question is whether their results clear a statistical bar high enough to separate skill from luck.

This three-part series is your roadmap. Read to the end of Part 3 and you'll know how to run a mathematical test, using IFA's calculator, to evaluate historical manager performance yourself.

We remember names, not data sets. A charismatic portfolio manager with a glossy track record is the investment world's version of a championship coach — quotable, confident, and credited with every win. From large-cap stock-pickers to macro hedge-fund titans, the story is seductive: special insight, repeatable edge, genius at work.

But admiration isn't analysis. In investing, stories travel faster than statistics. Before entrusting a hero with our life savings, we should ask a sobering question: are we seeing skill, or randomness dressed as brilliance? By the end of this series, you'll understand the methodology behind testing such claims.

How Star Managers Became Financial Celebrities

Star culture didn't happen by accident. It's the product of three forces working together.

Marketing that personalizes performance

Funds are sold through people. Manager letters, interviews, and conference appearances humanize complex strategies and make success feel attributable to a single mind. The halo effect kicks in: when we like the messenger, we over-credit the message.

Media that elevates outliers

News rewards the unusual. A manager who trounces a benchmark for a few years is, by definition, newsworthy. But what makes for a great headline — a streak, a bold call, a winning bet — rarely says much about durability.

Psychology that craves coherence

Our brains prefer tidy stories to messy data. We see patterns in small samples, assume brief streaks will last, and overestimate anyone's control over markets. One market cycle can crown one manager a genius and leave an equally skilled peer invisible.

Add the paradox of skill: as professional standards rise, true differences in ability shrink, leaving luck to decide who stands out. In a field of near-equals, tiny bounces determine the podium.

The Problem with Star Power: When Luck Masquerades as Skill

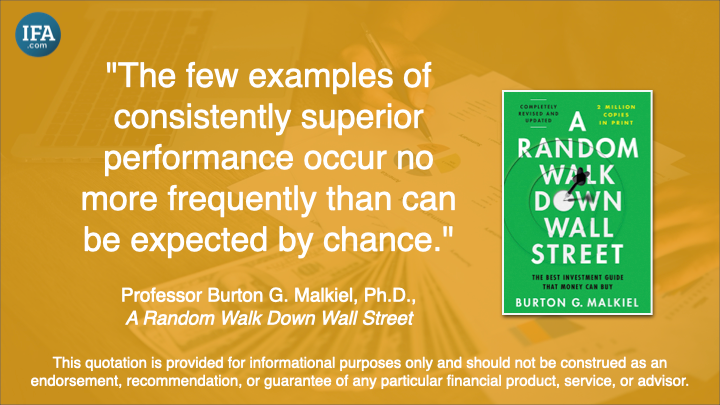

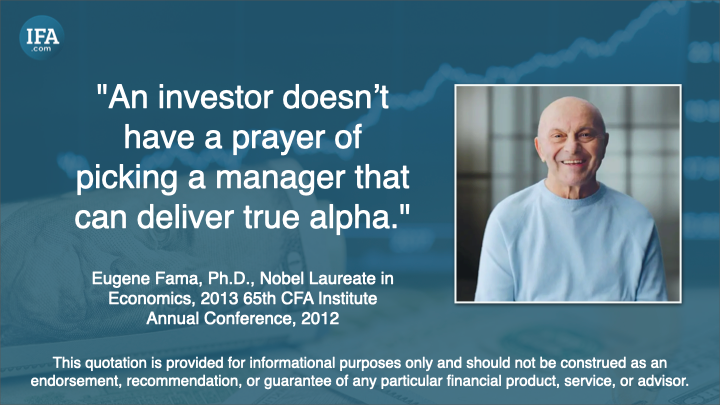

Decades of research pose an uncomfortable challenge to the star narrative. Once you adjust for risk, fees, and chance, persistent outperformance is rare.

● Jensen (1968) found that, after adjusting for risk, mutual fund managers did not deliver positive alpha on average.

● Sharpe (1991) demonstrated the arithmetic of active management: before costs, investors as a group earn the market return; after costs, the average dollar in active management must underperform. It's not cynicism — it's basic math.

● Carhart (1997) showed that what looks like skill often reflects exposure to known factors, and persistence in raw returns largely disappears once those are controlled for.

● Fama and French (2010) tested whether mutual-fund alpha exceeds what luck alone might produce. They found a small minority of funds with evidence of skill — but far fewer than casual observation suggests, and most gains vanish after fees.

Put simply, strong short-term results don't prove skill. Without a statistical test, we can't tell whether a manager's past edge is meaningfully different from zero. For instance, the Persistence Scorecard from S&P Dow Jones Indices shows that nearly all managers who outperform over one period fail to repeat it in the next.

Why Stories Beat Statistics — and How Investors Get Swayed

If the evidence is so clear, why do we keep believing in stars?

We remember winners and forget the field

Survivorship bias ensures we hear from the funds that lived to tell the tale. Hundreds of quiet closures never make headlines. We mistake visibility for validity.

We anchor on streaks

Markets cluster success. Even fair coins produce long runs of heads. When we see a three-year streak, we narrate genius instead of asking how common such streaks are across all managers. As Morningstar's analysis of winning funds turning cold shows, the "hot hand" often fades once investors pile in.

We confuse boldness with edge

Confidence sounds like insight. A gutsy macro call or concentrated stock pick can pay off for a time. The seductive leap is believing it was inevitable — and repeatable.

We underestimate the drag of costs

Even small fees compound into large hurdles. Any edge must pay management fees, trading costs, and taxes before reaching investors. Those frictions often turn "almost significant" results into statistical noise. As Mark Hebner explains in Step 3 of his award-winning book, The 12-Step Recovery Program for Active Investors, superior performance over time among stock pickers is usually a matter of luck, not lasting skill.

The point isn't to disparage professionals. Most are highly skilled and work extraordinarily hard. The point is that it's very difficult to beat the market with any consistency — and investors' best defense is to demand evidence that clears a statistical bar, not a storytelling one.

What Counts as Evidence? A Preview of Statistical Significance

You don't need to be a statistician to grasp the core idea. When a result is statistically significant, the outperformance is unlikely to be explained by random variation alone. In practice:

● Enough data: A few quarters won't do. Longer periods and more observations strengthen any test.

● A fair benchmark: Compare like with like. If a fund has a small-cap or value tilt, the yardstick should reflect it; otherwise you're rewarding exposure to known risks.

● After-cost reality: Test net of fees, because fees are what investors actually earn.

For a closer look at how these tests work, see IFA's Investor Guide to Financial Statistics, which explains how t-statistics separate genuine results from noise. Later in this series, we'll unpack what this means in plain language — how p-values, t-statistics, and Type I errors fit together — and why repeated "alpha hunts" raise the bar for proof.

From Hero Worship to Hypothesis Testing

If a manager's record intrigues you, great — now test it. Instead of outsourcing conviction to headlines or marketing decks, you'll have a repeatable way to evaluate claims. You won't just admire performance — you'll know whether it's likely to be repeatable. To preview the math behind it, see Calculations for T-Statistics.

A note on access and expectations

Some of the most publicized "stars" run vehicles unavailable to most investors, such as hedge funds. Even when access isn't an issue, the key question is the same: does the evidence support skill after costs with enough margin to reject luck? Until you run the numbers, treat confidence as a hypothesis, not a conclusion.

Luck and Skill: Learn to Tell the Difference

Follow this series and you'll gain:

- a clear understanding of why luck often looks like skill (Part 2); and

- a hands-on walkthrough showing exactly how to test any manager's results using IFA's calculator (Part 3).

Investing is hard because reality is statistical, not cinematic. The good news: the tools to tell the difference are simple — and they're in your hands.

Resources

Carhart, M. M. (1997). On persistence in mutual fund performance. Journal of Finance, 52(1), 57–82. https://doi.org/10.1111/j.1540-6261.1997.tb03808.x

Fama, E. F., & French, K. R. (2010). Luck versus skill in the cross-section of mutual fund returns. Journal of Finance, 65(5), 1915–1947. https://doi.org/10.1111/j.1540-6261.2010.01598.x

Jensen, M. C. (1968). The performance of mutual funds in the period 1945–1964. Journal of Finance, 23(2), 389–416. https://doi.org/10.2307/2325404

Sharpe, W. F. (1991). The arithmetic of active management. Financial Analysts Journal, 47(1), 7–9. https://doi.org/10.2469/faj.v47.n1.7

ROBIN POWELL is the Creative Director at Index Fund Advisors (IFA). He is also a financial journalist and the Editor of The Evidence-Based Investor. This article reflects IFA's investment philosophy and is intended for informational purposes only.

DISCLOSURES:

This content is for informational purposes only and does not constitute investment advice, an offer, or a solicitation to buy or sell any security. We recommend consulting a fiduciary or qualified financial advisor before making any investment decisions to ensure alignment with personal financial goals, risk tolerance, and circumstances. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. Examples are for illustration only. Any references to specific managers or funds are not recommendations and are provided solely to discuss general principles. Benchmarks are unmanaged and cannot be invested in directly.

IFA does not endorse or guarantee the accuracy of third-party content

For additional information about IFA, including detailed information about services, compensation, and potential conflicts of interest, please review our brochure available both at www.adviserinfo.sec.gov and www.ifa.com.

X

X